The English investment company Agronomics participates in companies that are involved in sustainable food. There are more than twenty interests in the portfolio, including two Dutch.

The focus is on cultivated meat and the production of vegetarian proteins, oils and fats through precision fermentation. The production costs are the biggest obstacle to the breakthrough of cultivated meat.

When Maastricht professor Mark Post showed the world the very first artificially cultivated hamburger in 2013, the production costs were the equivalent of about $1 million per kilo. However, the costs are decreasing exponentially, so that market experts estimate that cultivated meat will reach a market share of 10% as early as 2030. Because Agronomics is currently trading at a discount of almost 35% to its net asset value, it is now possible to speculate on this promising, sustainable sector at an attractive discount.

The market for cultured meat and vegetarian meat

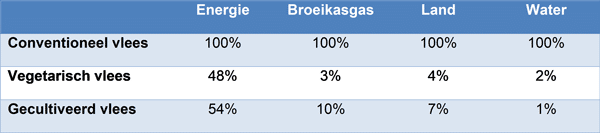

Conventional food production is responsible for a staggering 26% of global greenhouse gas emissions, which is more than all forms of transportation combined. Large parts of the Amazon and other rainforests have been cleared for cattle ranching and soy production. There are therefore many gains to be made with sustainable solutions for food production. Table 1 shows that the sustainable production of vegetarian meat substitutes and cultivated meat requires up to 50% less energy compared to traditional meat production. Greenhouse gas emissions can be reduced by 90% to 97%, up to 99% of drinking water can be saved and only a fraction of the land currently used for traditional livestock farming is needed. In addition to these clearly quantifiable benefits, there are other benefits, such as preventing animal suffering, reducing the use of antibiotics and preventing epidemics.

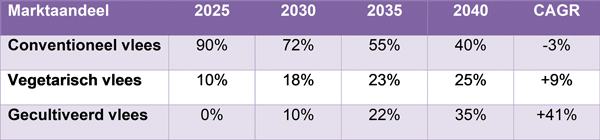

Due to the numerous advantages that vegetarian and cultured meat offer in combination with a rapid decrease in costs, it is expected that their respective market shares will increase rapidly at the expense of conventional meat. This can be seen in Table 2. The market share of vegetarian meat substitutes will increase from 10% in 2025 to 25% in 2040. The market share of cultured meat will increase even faster; from 10% in 2030 to as much as 35% in 2040. The potential for vegetarian meat substitutes and cultured meat is therefore enormous.

Cultured meat & vegetarian proteins

As already mentioned, Agronomics focuses on companies that are active as developers and producers of cultivated meat and of vegetarian proteins, oils and fats. With cultivated meat, the process is as follows: stem cells are isolated from a biopsy of an animal and with the help of a growth medium, oxygen and water, the stem cells multiply into a piece of meat. This is therefore not a meat substitute, because with the same building blocks, cultivated meat is identical to conventional meat. The vegetarian proteins, oils and fats are obtained by precision fermentation, or the stimulation of genetically modified bacteria and fungi.

The portfolio

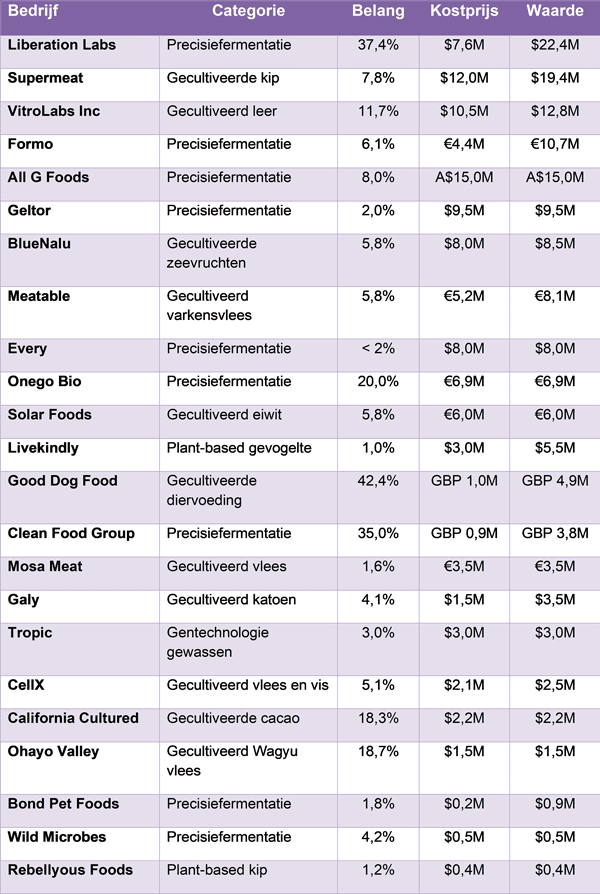

Table 3 shows an overview of the portfolio. In addition to the activities just mentioned, there are also interests in cultivated leather, cultivated seafood, cultivated cotton and cultivated cocoa. There are two Dutch interests: Mosa Meat and Meatable. Mosa Meat is the Maastricht-based start-up founded by the aforementioned Mark Post and Meatable in Delft was founded by Daan Luining, among others. Mosa Meat in particular has received a lot of publicity due to the support of Sergey Brin, one of the founders of Google, among others. The founder of Thuisbezorgd, Jitse Groen, and Leonardo DiCaprio are also shareholders in Mosa Meat.

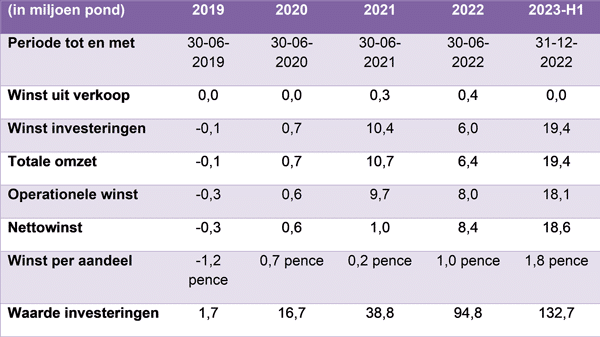

Results

Please note: the financial years are broken and run from 1 July to 30 June.

Table 4 shows the results from 2019 onwards. The turnover is formed by realised and unrealised profits and losses, so that it is in fact about the value development of the portfolio interests. Given that there has been a lot of interest in sustainably produced food in recent years, it is not surprising that the value development of the portfolio has been favourable in the past period.

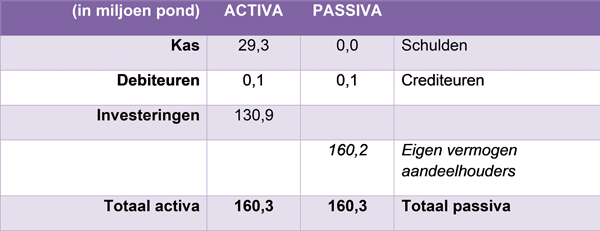

The financial position

Table 5 shows that the company is debt free. The cash position is generous at £29.3m. There are no intangible assets, which means that the equity of £160.2m is equal to the net asset value (NAV), or 16.1p per share. The balance sheet is certainly solid.

Potential dilution, nearly 440 million warrants

There are almost 440 million warrants outstanding, which could mean significant dilution on the total number of outstanding shares of around 992 million. A closer look shows that 297 million warrants have an exercise price of 28.5 pence and an expiry date of 1 June 2024. In addition, 137 million other warrants have an exercise price of 30 pence and an expiry date of 8 December 2024. Given that the current price is barely 10 pence, this dilution will only come into play if the price increases by more than 200%.

Potential dilution, nearly 440 million warrants

The world of sustainable food production is similar to that of biotechnology. It revolves around intellectual property that is well protected and, as in biotechnology, it is difficult to predict which company will be successful. Agronomics seems to have found a nice formula by choosing a portfolio of around twenty interests with a team of sector specialists, which significantly reduces the risk in this speculative sector. With the successful British investor Jim Mellon on board, who not only has a stake of over 15% but is also part of the executive management, Agronomics has a heavyweight on board.

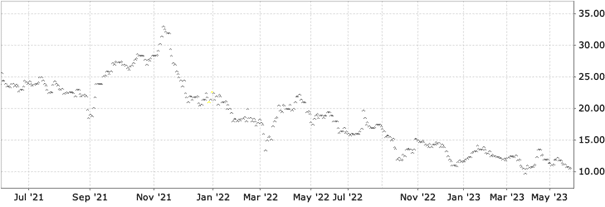

The opportunity to enter with a discount of around 35% on the NAV seems like a golden opportunity. Investors should keep in mind that despite the good diversification of interests in the portfolio, an investment in Agronomics is speculative. On the other hand, very high price gains are possible if one or more interests prove to be successful.

Key Facts

Name: Agronomics Limited

Ticker: ANIC

Exchange: London Stock Exchange (LSE)

ISIN: IM00B6QH1J21

Price: 10.5 pence

52-week low: 9.6 pence

52-week high: 20.5 pence

Price GBP.USD: 1.2370

Number of shares outstanding: 992 million

Market capitalisation: £104.2 million

Cash position: £29.3 million

Total debt: nil

Net worth: £29.3 million

Enterprise value (EV): £74.9 million

Net asset value (NAV): £160.2 million

NAV per share: 16.1 pence

Price/NAV: 0.65x

Dividend per share: 0.0 pence

Major Shareholders

Jim Mellon: 15.4%

Hargreaves Lansdown: 8.7%

BlackRock Inc: 6.3%

Canaccord Genuity: 5.8%

Interactive Investor Services: 5.1%

JPMorgan Chase Bank: 4.0%

Jupiter Asset Management: 2.6%

Website

www.agronomics.im