Last week, CM.com received a buy recommendation from analysts at ING Group with a target price of €12. The price has since risen above €10. The stock market, on the other hand, is faltering. Although the price could still go a bit higher, no one has ever become poorer from taking profits. We are selling our entire position in CM.com with a profit of approximately 22%. At the same time, we are investing in the company Allego NV, of which we are including 400 shares in the portfolio of Aandelenondereentientje at the current price of approximately $2.22. Below you can find the entire analysis of Allego.

Analysis: Can Allego charge investors for returns?

Allego benefits from the European ambitions to electrify the vehicle fleet and has become one of the largest European charging station operators. Europe wants to significantly expand the number of charging points in the coming years and stimulate the sale of electric cars. The growth potential of the charging station sector has led to fierce competition.

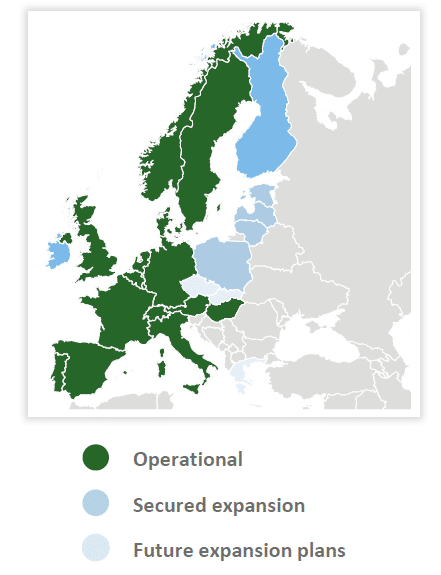

Dutch energy grid operator Alliander founded Allego in 2013 to respond to the electrification of the vehicle fleet. Allego builds and operates charging stations and provides services to third parties, including billing and maintenance of charging points. In 2018, French investment fund Meridiam acquired Allego from Alliander. A few years later, they chose to list the company on the stock exchange in America rather than in the Netherlands. On March 17, 2022, Allego was listed on the Nasdaq via the SPAC (special purpose acquisition company) of private equity firm Apollo Global Management. The IPO raised Allego $500 million and the company was valued at $3.14 billion. Allego now operates one of the largest public charging networks for electric cars in Europe. The company is active in a large part of Europe and plans to expand further in Eastern Europe in the coming period. Allego works with Shell, Nissan and Carrefour, among others, with which it has concluded lease contracts that usually have a term of ten to fifteen years.

Strong growth

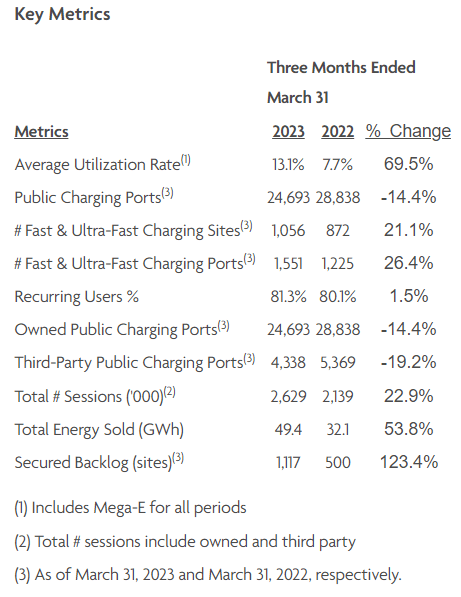

In the first quarter of 2023, Allego’s revenue increased by 27.4% year-on-year to €38.8 million. Thanks to significant growth in the number of operational chargers combined with price increases, revenue from the charging division increased by 166.7% to €27.8 million. The average occupancy rate of the charging points increased from 13.1% to 70% and the number of charging sessions increased by 23% to 2.6 million. In the service division, revenue decreased from €20 million to €10.9 million, mainly driven by lower revenues from a project with Carrefour. Operating EBITDA amounted to €8.9 million, compared to €1.5 million a year earlier. Gross profit improved by 190.9% to €13.4 million and the net loss decreased from €351 million to €13.2 million. In the first quarter of 2022, Allego incurred one-off costs in connection with the stock exchange listing. In order to reduce its exposure to volatile energy prices, Allego signed 160 GWh of renewable energy contracts. The number of prime location contracts increased from 500 to 1,300 last year and the network will be further expanded in the coming period. Allego announced at the end of February that it had agreed with Swedish real estate company Trophi to install 32 public charging stations at its shopping centres this year. At the end of May, Allego announced a partnership with the porta Group, a German family-owned furniture company. Allego will install a total of 1,500 charging points at 123 locations of the porta Group, so that consumers can charge their electric cars while shopping. The charging stations will have both fast (50 kW) and ultra-fast (150 kW) charging points. Allego reiterated its previous guidance for 2023, in which it expects a turnover of €180-220 million and an operating EBITDA of €30-40 million.

Electrification of the vehicle fleet

Allego can benefit from the European ambitions to make the vehicle fleet more sustainable. Earlier this year, a proposal was made in Europe to amend the Alternative Fuel Infrastructure Regulation (AFIR). The new rules stipulate that from 2026, there must be a fast-charging station of at least 150 kW every 60 kilometres along European motorways. If the new plans go ahead, the number of charging points in Europe must grow from the current 450,000 to 3.4 million in 2030. According to research agency McKinsey, €40 billion is needed to achieve this. Furthermore, the Dutch government plans to oblige lease drivers to opt for an electric car from 2025. The Dutch government also wants every new car sold from 2030 to be an emission-free car, in order to reduce greenhouse gas emissions from the Dutch vehicle fleet. The European Union wants to ban the sale of new cars and vans with a combustion engine from 2035.

Growth restrictions

One of the risks to Allego’s growth is the electricity grid. According to research firm McKinsey, Europe will need around 2,800 TWh of electricity in 2030, of which 165 TWh will be used to charge electric cars, which represents 6% of total electricity demand. To meet the increasing demand for electricity, the European electricity grid needs to be improved. According to McKinsey, this investment will cost €41 billion, and to generate the amount of electricity needed to charge EVs, another €74 billion is needed. Another factor is that tendering procedures for new charging stations and obtaining a connection to the grid can take up to two years. In addition to the capacity limitations of the European electricity grid, electricity prices could be a game changer. If demand for electricity grows faster than supply, it is likely that electricity prices will rise, making it less attractive for companies and consumers to electrify their fleet. In addition, subsidies for electric cars are gradually being phased out in various countries. Due to the increasing additional tax, an electric car in the Netherlands now costs on average just as much or even more than a petrol car. In addition, the exemption from motor vehicle tax that EV owners currently benefit from will disappear in the Netherlands from 2025. Electric cars are often heavy due to their battery pack, which can cause motor vehicle tax to rise considerably. The Electric Drivers Association is therefore advocating a weight correction for electric cars, so that the battery weight does not count towards motor vehicle tax. The Dutch government has indicated that it will not make any changes to the policy for the time being, which means that EV drivers will have to pay motor vehicle tax from 2025 until at least 2030. The subsidies are also being rolled back in Norway. There, VAT must be paid if the electric car costs more than €50,000 and the owner of an EV now also pays motor vehicle tax. In addition, EV owners are no longer exempt from paying tolls on toll roads. There is a good chance that European governments will turn off the subsidy tap for electric cars in the event of a recession.

Chances:

- In the coming years, Europe will invest heavily in the installation of charging stations, which offers Allego the opportunity to win new contracts.

- The further electrification of the European vehicle fleet will lead to more charging sessions.

- Longer lease terms provide stable income streams.

Threats:

- Allego faces fierce competition, including from FastNed and Alfen.

- The charging station specialist is heavily dependent on government policies in countries for its growth. In the event of a recession, investments by European governments can decline significantly.

- Volatile energy prices impact Allego’s performance.

Conclusion

Allego is in a market that is expected to continue to grow rapidly in the coming years due to the further electrification of the vehicle fleet. The charging station specialist has concluded a number of interesting contracts and showed strong growth in results in the first few months. However, the company is still making a loss and the share price has not or hardly responded to the first-quarter figures. We believe that investors are underestimating the share and find the current price level so low that a buy recommendation is justified. We are therefore including 400 shares of Allego NV in the portfolio of Aandelenondereentientje at the current price of around $2.22. We set the target price at $3.50.

At the time of writing, the author has no position in Allego.

Fundamental characteristics Allego NV

ISIN code: NL0015000TA9

Ticker: ALLG

Sector: Electrical components

Exchange: Nasdaq

Price June 6: $2.20

Free float: 267.178 million

Number of outstanding shares: 267.178 million

Market capitalization: $585.119 million

Price high last 12 months: $8.01

Price low last 12 months: $1.85

Website: https://ir.allego.eu/