On May 5, Intesa Sanpaolo, Italy’s largest bank, raised its full-year profit outlook, citing a doubling of net profit in the first quarter, thanks to higher interest rates and shrinking loan loss provisions.

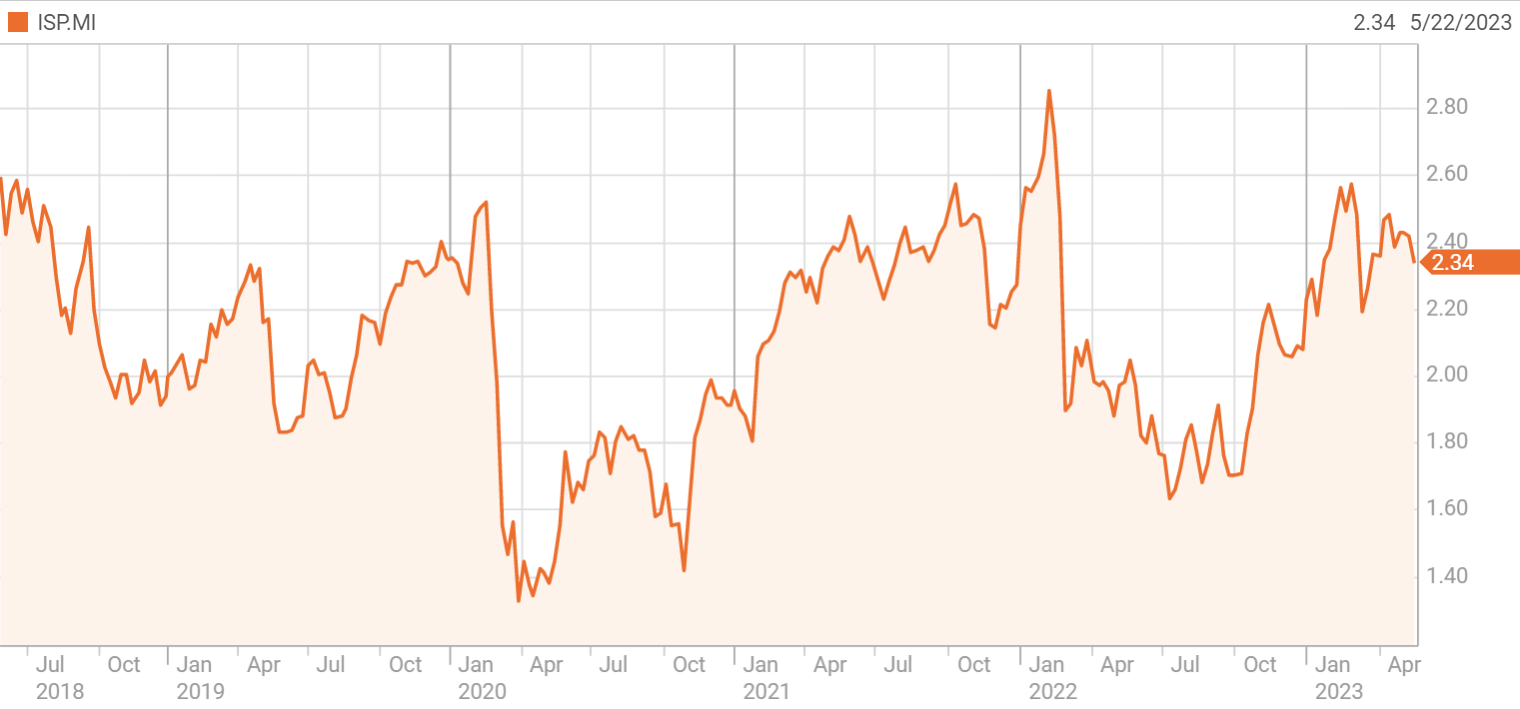

Based on a price-earnings ratio of around 11 and 6.5 for 2022 and 2023 respectively, the share is not overvalued, while the dividend yield of 6.7% supports the share price. In addition, there is a good chance that Intesa Sanpaolo will launch a share buyback program. In our opinion, these positive factors are not sufficiently reflected in the share price. We are therefore including 1,000 shares of Intesa Sanpaolo SpA in the portfolio of Aandelenondereentientje at the current price of 2.34 euros per share. The bank can continue to benefit from (even) higher interest rates and we believe that the price can then rise even further.

Profile

With a market capitalisation of around €45 billion, the Intesa Sanpaolo Group (Intesa) is one of the largest banking groups in Europe and is the market leader in Italy in all business areas (retail, corporate and asset management). The bank serves its 13.6 million customers through a network of around 3,500 branches spread throughout the country. Internationally, Intesa is present in the commercial banking sector through subsidiaries with over 950 branches in twelve countries in Central and Eastern Europe, the Middle East and North Africa, where it has 7.1 million customers. A network of specialists also advises the bank’s corporate clients in 25 countries.

As Italy’s largest bank, Intesa is preparing for the digital age. The bank is investing €5 billion in new technology until 2025, of which €650 million is earmarked for the digital platform Isybank. Intesa is working with the English Thought Machine over the next five years to develop this new digital bank. Intesa wants to serve 4 million of its ‘young’ customers online using mobile banking services. In the field of digital banking, Italy lagged behind other European countries with its ageing population and the bank wants to do something about that . In anticipation of the launch of the new digital bank, Intesa has already closed more than 550 branches since the end of 2021. The bank hopes to have reduced its operating costs by €600 million by 2025, an amount that should increase to an annual saving of €800 million.

Numbers

The quality of the figures at this bank is beyond reproach. Analysts and investors were impressed by the latest results. Intesa reported a net profit of €1.96 billion for the first quarter, significantly higher than the forecasts of Reuters analysts, who had expected a net profit of €1.54 billion. Total revenue also exceeded expectations, coming in at €6.06 billion, up 7% from the fourth quarter of 2022. Higher interest rates led to a 66% year-on-year increase in loan income.

As much of Intesa’s business is focused on asset management and insurance, the bank has been more affected by the unrest in the banking sector in recent months than its rival UniCredit. However, the bank has benefited greatly from rising interest rates and the quarterly report underlined that earnings will continue to benefit from this in the coming quarters. Net interest income is expected to exceed €13 billion this year and this forecast has allowed the full financial year to be raised significantly. The bank also confirmed its dividend payout ratio of 70%, ensuring that shareholders can continue to count on their dividend.

Pros:

- Banks are benefiting from the higher interest rates.

- In terms of profitability, Intesa Sanpaolo is showing considerable resilience.

- The implementation of the 2022-2025 business plan is well on schedule.

Cons:

- Uncertainty about the economy remains a limiting factor in the banking sector.

- The focus on asset management and insurance makes Intesa more vulnerable than its peers.

- The Italian government is considering an additional tax on profits made by banks.

Conclusion

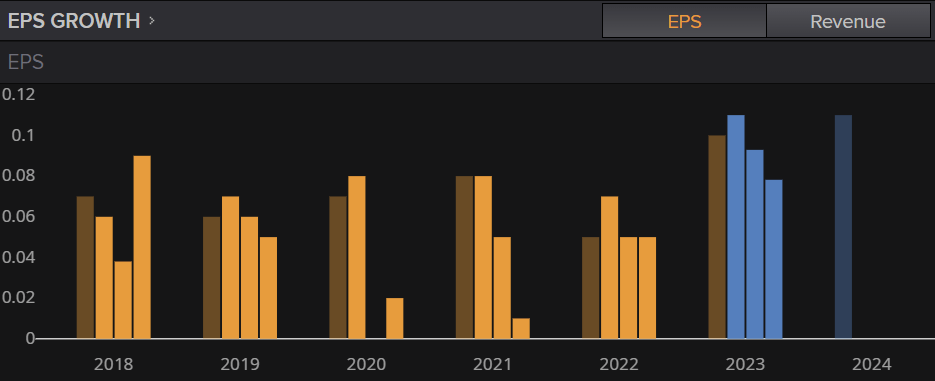

The outlook for the 2023 financial year looks very positive. Intesa should be able to benefit from the higher interest rates in the eurozone, especially now that the European Central Bank plans to raise the base rate further. The effect of the increased interest rates should also be noticeable in the years after 2023. The bank is forecasting a net profit of €7 billion for 2023, where previously it had assumed a profit that would be slightly higher than the profit of €5.5 billion achieved in 2022. Where the 2022-2025 business plan still assumed a net profit of €6.5 billion for 2025, this will be far exceeded, according to CEO Carlo Messina.

The fundamentals for the Italian banking sector look excellent and both Intesa and peer UniCredit raised their profit target for 2023 by more than 20%. The increase in profit forecasts is largely due to the fact that the reserves for possible credit losses have been revised downwards.

However, this positive coin also has a downside. At a time when households are under pressure due to the sharp rise in the prices of basic necessities, it does not seem appropriate for banks to make so much profit. Following Spain’s example, the Italian government is therefore considering imposing an additional profit tax on banks. CEO Messina said that Intesa would support such a measure, provided that it is a one-off measure aimed at helping people in need.

Because Intesa is also increasingly present abroad, the risks are not limited to the domestic market. With its international division International Subsidiary Banks, Intesa achieved an annual growth of almost 7% in total assets over the past three years. International Subsidiary Banks is active in twelve countries, including China, where it operates through the Chinese asset manager Yi Tsai. Intesa also has a minority interest in Penghua Asset Management and Qingdao Bank.

Intesa has been affected by the unrest in the banking sector in recent months. In the United States, several regional banks went under and in Europe, Credit Suisse had to be rescued by UBS. Although the future looks good for Intesa, the stock price has been somewhat slowed down by these bankruptcies.

Based on a price-earnings ratio of just under 11 for 2022 and an estimated 6.4 and 6 for 2023 and 2024 respectively, the share is certainly not overvalued. The attractive dividend yield of 6.7% and the possible buyback of own shares can support the share price. The analysts at Aandelenondereentientje are closely following the share and will not hesitate to take profits if the opportunity arises. For now, we are adding 1000 shares of Intesa Sanpaolo SpA to our portfolio at the current price of €2.34.

Fundamental characteristics Intesa Sanpaolo SpA

ISIN code: IT0000072618

Ticker: ISP.MI

Exchange: Euronext Milan

Earnings per share 2022: €0.23

Tax. earnings per share 2023: €0.37

Tax. earnings per share 2024: €0.39

Tax. price/earnings ratio 2023: 6.5

Price on May 19: €2.33

Price high of the last 12 months: €2.60

Price low of the last 12 months: €1.58

Dividend: €0.16

Dividend yield: 6.70%

Number of shares outstanding: 18.26 million

Market capitalization: €44.83 billion

Sector: Banks

Book value per share: €3.25

Debt: €257.79 billion

Website: group.intesasanpaolo.com