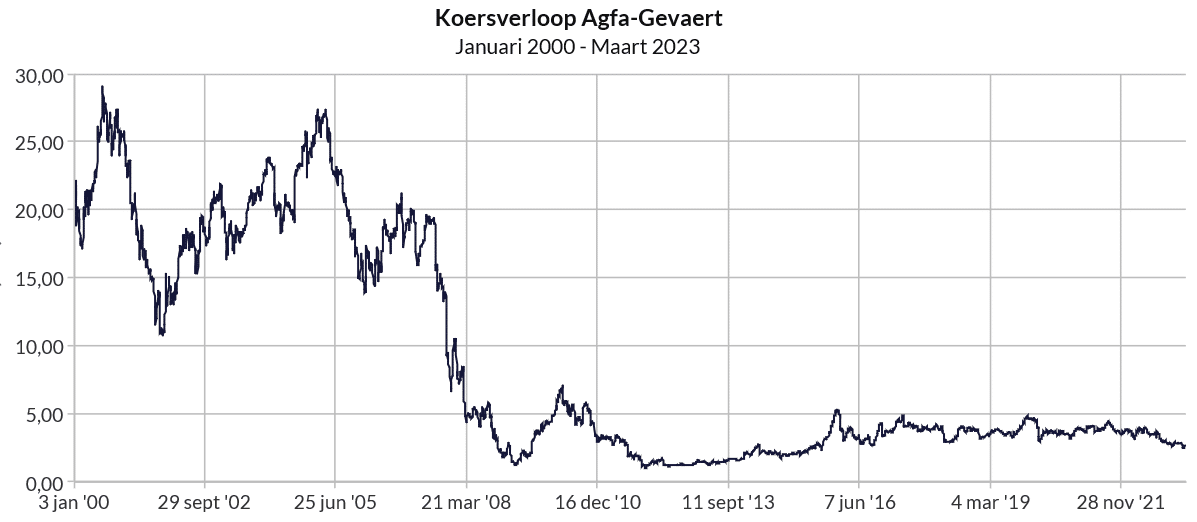

After years of reorganizations, there is a ray of light on the horizon for the Belgian Agfa-Gevaert. Next month, the sale of the offset division will be completed, which could lead to the first profit being made this year. The real turnaround should then take place in 2024, the year in which the offset division will no longer be included in the annual accounts for the first time. The risk profile for Agfa-Gevaert remains high, however, and management still has to prove that the cash flow can also grow autonomously. In the past, this cash flow only increased because new credits were taken out and subsidiaries were said goodbye to that no longer fit the company profile.

Sharesunderonetientje is not waiting for the half-year figures and is now giving a buy recommendation. We believe that management will succeed in achieving the turnaround and consider a price increase of 50 to 100% possible. We are buying 1000 shares in the portfolio of Sharesunderonetientje at the current price of 2.66 euros.

Profile

Agfa-Gevaert (Agfa) develops, manufactures and distributes a wide range of analogue and digital imaging systems for the graphic industry, the healthcare sector and specific industrial applications. After the divestment of Agfa Photo, the company has become a pure B2B player. The world-leading imaging technology company employs around 8,000 people and can look back on more than 150 years of experience. The group operates through four divisions: Radiology Solutions, Healthcare IT, Digital Print & Chemicals and Offset Solutions. In April, the Offset Solutions division will be sold to Aurelius Group, but management continues to look for promising new activities.

In March 2022, it was announced that an investment would be made in a new Zirfon membrane plant for the production of green hydrogen and that the existing plant would be expanded. The new plant, which will be located in Mortsel, Belgium, is designed in such a way that a possible expansion in the future is possible. Pascal Juéry, CEO of Agfa-Gevaert, explained the investment as follows: “This demonstrates our commitment to the energy transition and the decarbonisation of industrial and transport activities. This investment is fully in line with the EU’s ambitions to build a strong European hydrogen economy and to produce 10 million tonnes of hydrogen locally by 2030 under RepowerEU.”

Figures

The Agfa-Gevaert Group did not escape the adverse market conditions in 2022, such as continued cost inflation, lockdowns in China and weaker demand in markets outside healthcare. Compared to 2021, adjusted EBITDA decreased by 9% and the bottom line was a net loss of €223 million, mainly due to non-cash impairments at the Radiology Solutions and Offset Solutions divisions. The profitability of the Radiology Solutions division suffered from the pressure on margins and volumes sold in China. Revenue growth was achieved in Digital Print & Chemicals, but here too profitability was strongly under pressure due to cost inflation and one-off effects. Things improved at the HealthCare IT division, as more momentum was created there. The turnaround was achieved in Offset Solutions and the sale to Aurelius is still on track for the first week of April.

Pascal Juéry commented on the annual report: “2022 was a year of unprecedented economic and geopolitical instability. Cost inflation, supply chain disruptions and Covid lockdowns impacted our activities. Particularly in these turbulent times, we continue to execute on our strategic agenda. Our priorities for 2023 are to implement further price increases across all our activities, reduce costs based on business model initiatives and deliver growth in HealthCare IT, Zirfon and digital printing.”

Expectations

Agfa-Gevaert performed very moderately in the fourth quarter of last year and the profit at EBIT level was even considerably lower at €5 million than the expected €14 million. The guidance sounded optimistic and a general improvement in profitability at group level was forecast for the current financial year. Radiology Solutions, the company’s most valuable division, will probably be able to present better than expected results. On the other hand, the outlook for the Digital Print & Chemicals division looks less promising. The guidance for this last division will probably have to be adjusted downwards and it is still uncertain what will weigh most heavily in the final settlement. Stable performance can be expected from the HealthCare IT division. The offset division will still account for a maximum of one third in the annual figures in 2023 and the results of this division will only be excluded from the final settlement next year.

Opportunities:

– The company benefits from higher interest rates that reduce pension costs.

– The handicap of the lack of growth of the autonomous cash flow seems (almost) solved.

– Sale of the offset department lightens the financial position.

Risks:

– The risk profile remains high.

– Management will have to prove that cash flow can also grow autonomously.

– After the sale of the offset department, 2024 will be the year of truth.

Conclusion

After years of reorganizations and the sale of non-core activities, Agfa should be ready for a new future. The sale of the Offset division to Aurelius Group should allow Agfa to focus on growth in the remaining activities. This year, the priority is to implement price increases in order to absorb the increased costs and to further reduce those costs. After another loss-making 2022, management expects 2023 to be the year of return to profitability.

Next year will be the year of truth, because then the results of the offset division will no longer be included in the annual accounts for the first time. The management will then have to prove that it can also grow the cash flow autonomously and that a profit can indeed be realised at the bottom line. The cash flow has only been positive in recent years because new credits were taken out and subsidiaries that no longer fit the company profile were said goodbye to.

Sharesunderonetenth is not waiting for the half-year figures to get the share on board. We are therefore already giving Agfa-Gevaert a buy recommendation because the share should be able to withstand higher prices if the half-year figures turn out positive. In our view, the risk of decline is limited, which, for what it is worth, gives a safer feeling. The upside potential for this laggard is great and we do not rule out a price increase of 50 to even 100%. We are buying 1000 shares in the portfolio of Sharesunderonetenth at the current price of 2.66 euros.

Fundamental characteristics Agfa-Gevaert

Earnings per share 2022: –

Tax. earnings per share 2023: € 0.05

Tax. earnings per share 2024: € 0.15

Price/earnings ratio 2022: –

Price at time of writing: € 2.60

ISIN code: BE0003755692

Ticker symbol: AGFB.BL

Price high last 12 months: € 4.16

Price low last 12 months: € 2.44

Dividend: –

Dividend yield: –

Number of shares outstanding: 154.8 million

Market capitalization: € 444.3 million

Sector: technology

Return on assets: -5.19%

Return on equity: -35.77%