Investors fear that interest rates will not go down this year, as was previously expected. Strong macroeconomic figures confirm economic growth, which is why some members of the American central bank (FED) would prefer to see an interest rate increase of 0.75% to quickly reduce inflation. Investors do not want to see such interest rate increases and we see this reflected in falling prices as a result. Why banks are also falling is a mystery to us, because banks actually benefit from rising interest rates. According to the Aandelenondereentientje team, it is a healthy cooling down because the stock markets are far ahead of the facts. Periods of profit-taking and doubts are then no more than normal.

In Germany, the purchasing managers index again contracted. The index fell from a level of 47.3 to 46.5 (A level above 50 means growth, below that means contraction). The European services sector, on the other hand, showed clear growth and rose to a level of 53, while last month a level of 50.8 was still on the boards. All in all, these were mixed figures that offer little support to investors. It doesn’t matter to us, we already buy shares under ten euros that are dirt cheap in our eyes.

We are currently working on a stock that we could buy for three quarters. It is quite a strange story and just this week all kinds of news came out that drove us back to the drawing board. But the most beautiful flowers grow along the edge of the ravine, so if we are going to pick them, you will be the first to know with an extensive analysis. For now time to discuss our portfolio.

Wallet

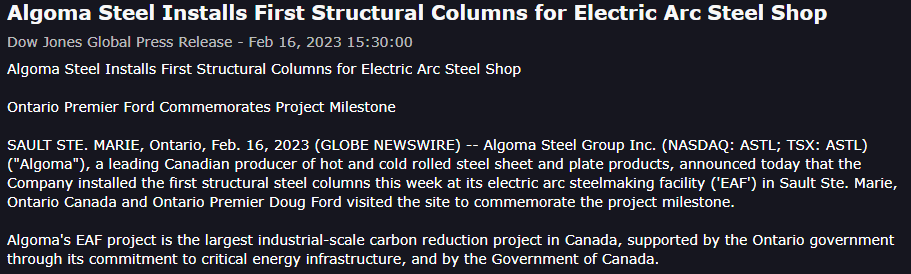

Algoma Steel Group Inc.: A few weeks ago we emailed you that we sold more than half of the shares (250 out of 400) and cashed in a nice profit of over 30%. A good choice, the share price has dropped a bit. But is that justified? The steel group recently reached a new milestone in the construction of its production facility in Sault Ste. Marie for so-called electric arc furnaces. The group’s project is the largest carbon reduction project on an industrial scale, because electric arc furnaces run on electricity. It is supported by both the governments of Canada and Ontario because it is part of the critical energy infrastructure. Given the importance of Ontario’s carbon reduction goal, the company is pleased to celebrate this important milestone and the Premier of Ontario even came to take a look. Combined with Ontario’s low-carbon electricity grid, the company expects that this transition will position Algoma as one of the leading producers of “green steel” in North America. The group is growing well and our team of analysts has full confidence in this company and is therefore holding the remaining 150 shares very firmly.

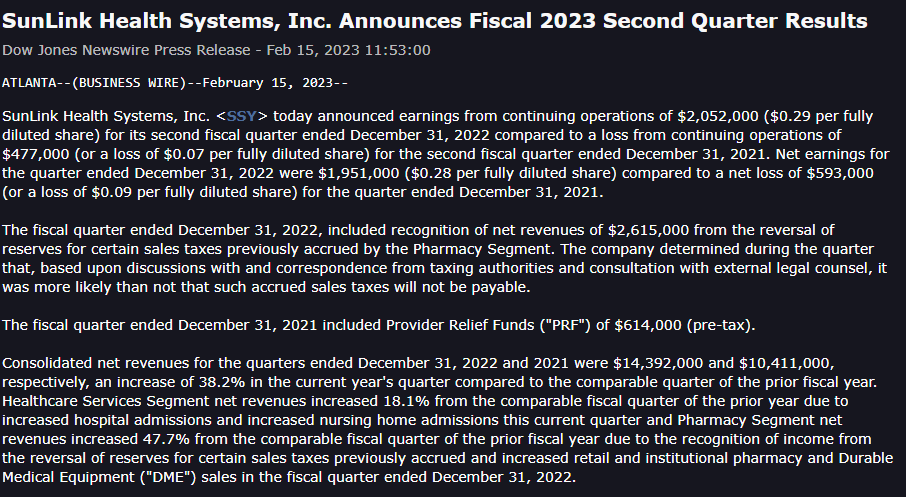

SunLink Health Systems, Inc.: this company has a number of hospitals and pharmacies plus a piece of land to develop them! The stock was still at a price of $4.83 a few years ago, to slide back for no reason to a current price of around $1.07. A new round seems to be on the way! The stock has already been somewhat lower, but when we tipped this stock at $0.85, it rose more than 20% to a price of $1.07 now. However, we have higher expectations for this stock. The company came up with strong figures and showed a profit per share of $0.28, while a loss of $0.09 per share was realized last year. The consolidated net income increased by more than 38.2% to an amount of $14.393 million, versus $10.411 million a year earlier. Our team of analysts is therefore very pleased with this and we are surprised by the lackluster price reaction to the figures. We are holding on to the shares firmly.

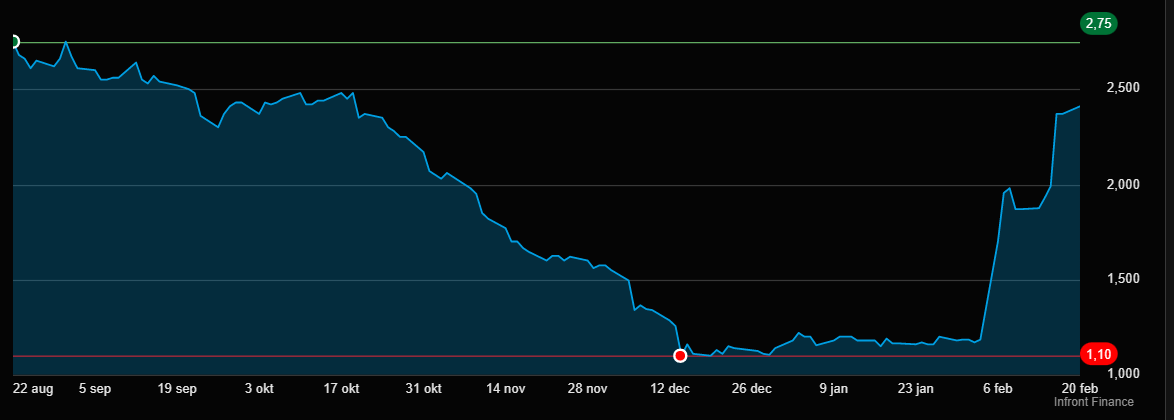

MotorK: hats off to the investors who bought this stock in time and now have a profit of around 25% on paper! MotorK seems to be coming out of the deep valley, but still has a long way to go. We indicated to buy limited shares of the stock, but we doubt whether all investors in this stock have done so. Fortunately, the price of the stock remains nice and firm, but smart purchasing requires discipline and patience. We aim for a higher price than the current one, keep an eye on our updates.

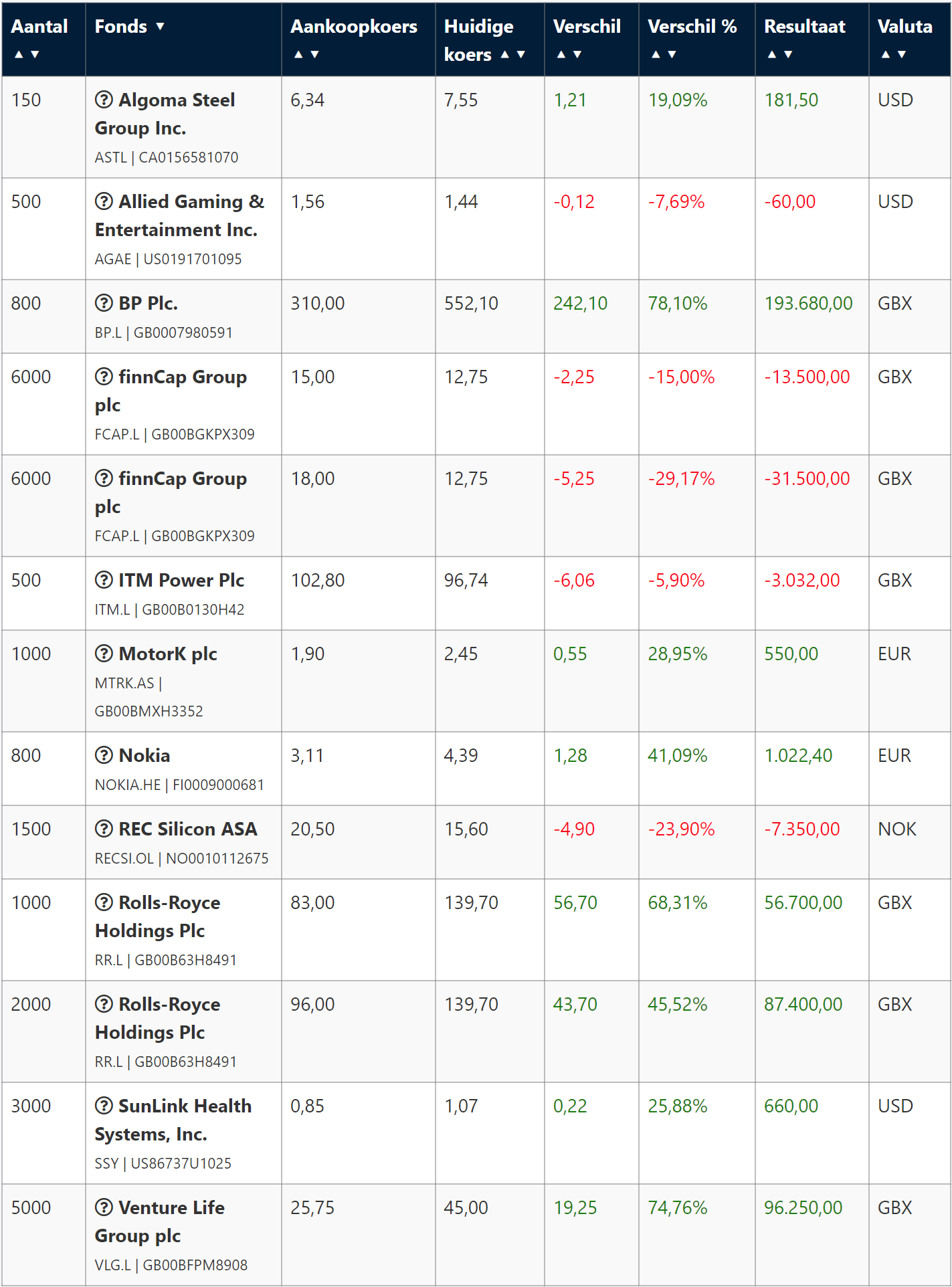

Finally, the portfolio overview: