The stock markets are still very strong. Investors are realizing that the global economy is doing better than previously feared. This is making the chance of a recession smaller and investors can happily invest their hard-earned money again. We also see this reflected in the growing number of subscribers to Aandelenondereentientje, investing in shares under ten euros – penny stocks – is becoming increasingly popular! We have a number of nice homeruns in the portfolio.

This week was an exciting week with no less than two interest rate decisions from America and Europe. In America, the interest rate was increased by 0.25% and in Europe by 0.50%. These interest rate decisions were already priced in by investors and the stock markets continue to find their way up. Positive news is also that European inflation is falling significantly to an annual inflation of 8.5%, where an inflation of 9.2% was expected. The Shares Under a Tenner portfolio is doing very well this week with many risers and that sets the tone for the entire year as far as we are concerned.

We have a new stock on the shelf and are busy with the layout. The stock costs about 85 cents and we have, if we say so ourselves, a good substantiation. Whether you buy an expensive or cheap stock, the analysis must always be sound and in-depth, that is what you can expect from us and that is why you are also a subscriber. You can expect the analysis soon. Read it carefully and check whether you agree with us, because you are ultimately the one who makes the decisions. Time to discuss our portfolio news. For example, we are selling a part of our shares in Algoma Steel Group.

Wallet

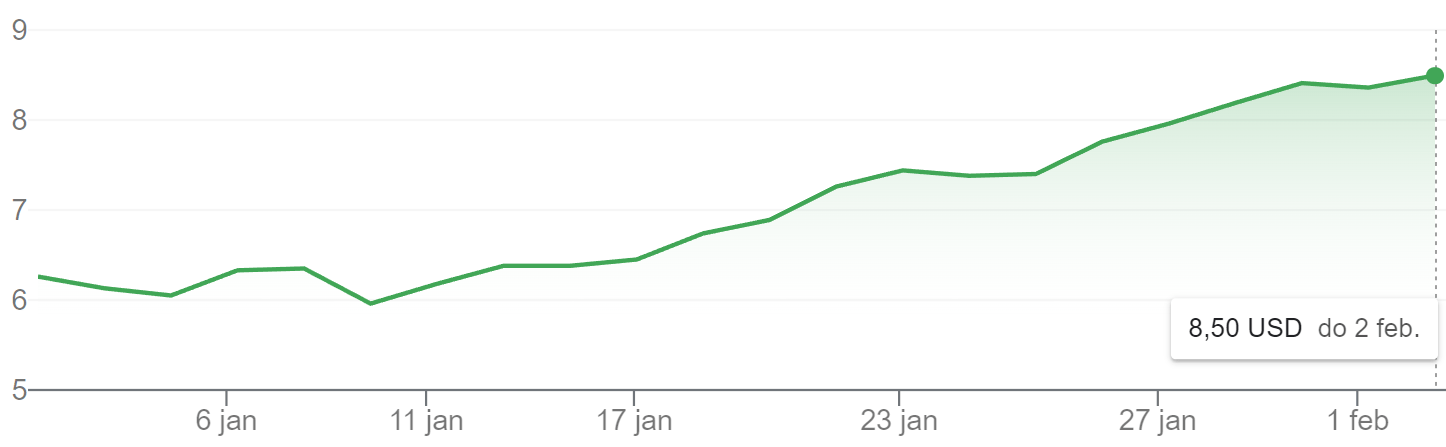

Algoma Steel Group Inc.: This share went faster than expected! It won’t be long before this share is no longer listed under ten euros, because the price has been rising for the past few weeks and is ‘still going strong’. Subscribers to Aandelenondereentientje have already made more than 30% profit on the share! It seems that this share is increasingly coming onto the radar of banks and it was about time! The growing company has been listed on the stock exchange for a year and a half, while the company has been around for over 100 years. Unknown makes unloved. Algoma Steel is making nice profits. We are going to be strategic and sell 250 of the 400 shares at around $8.48. That means a nice profit of 33% from our purchase price of $6.34 or $2.14 per share! We are then left with 150 shares and these will only cost us the equivalent of $2.77 per share. With these remaining shares we will seek the golden mountains and let them rise to levels that belong to shares above ten euros. For novice investors, this strategic thinking may require some calculation. Do this calmly and deliberately; those who are not strong must be smart.

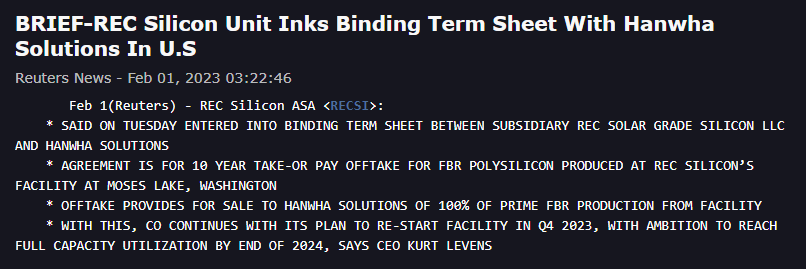

REC Silicon ASA: is considering reopening its already closed factory and the share price shot up 27% on this news, a good start to higher prices. The Norwegian producer of silane gas (used in the production of solar energy) announced a 10-year agreement with Hanwha Solutions, under which they will purchase the successful product FBR polysilicon. This purchase of large production levels like this has been a condition for the reopening of the already closed REC Silicon factory in Moses Lake. The purchase with Hanwha Solutions offers REC Silicon the necessary certainty to restart the closed factory in Moses Lake in order to gain a large market share in America. With this, the company makes large quantities of high-quality, ethically produced and low-carbon solar energy available, for which there is a strong demand. This will allow REC Silicon to grow even further, which has made the analyst team at Aandelenondereentientje even more enthusiastic about this share and we therefore maintain a strong buy recommendation on this promising share.

ITM Power Plc: the price of this volatile but promising share is like a bouncing ball. After the annual peak of around £4, the price has slipped back to a price of around £1 and we gave it a buy recommendation at the time. Fortunately, the price is now higher and rose by more than 10% today! The slipping price was caused by the management having to temporarily suspend the construction of a new factory, due to a challenging and uncertain market. As a result, the management has appointed a new CEO to keep the company on track and our team of analysts believes that if the new CEO delivers on all plans, the price can rise again. However, it is possible that we will also jump rope on this volatile price in the meantime. We will then email you this without delay. The new CEO is already taking good steps, because they are going to reduce the workforce by a quarter to significantly reduce costs, which will lead to a cost saving of £9 million per year.

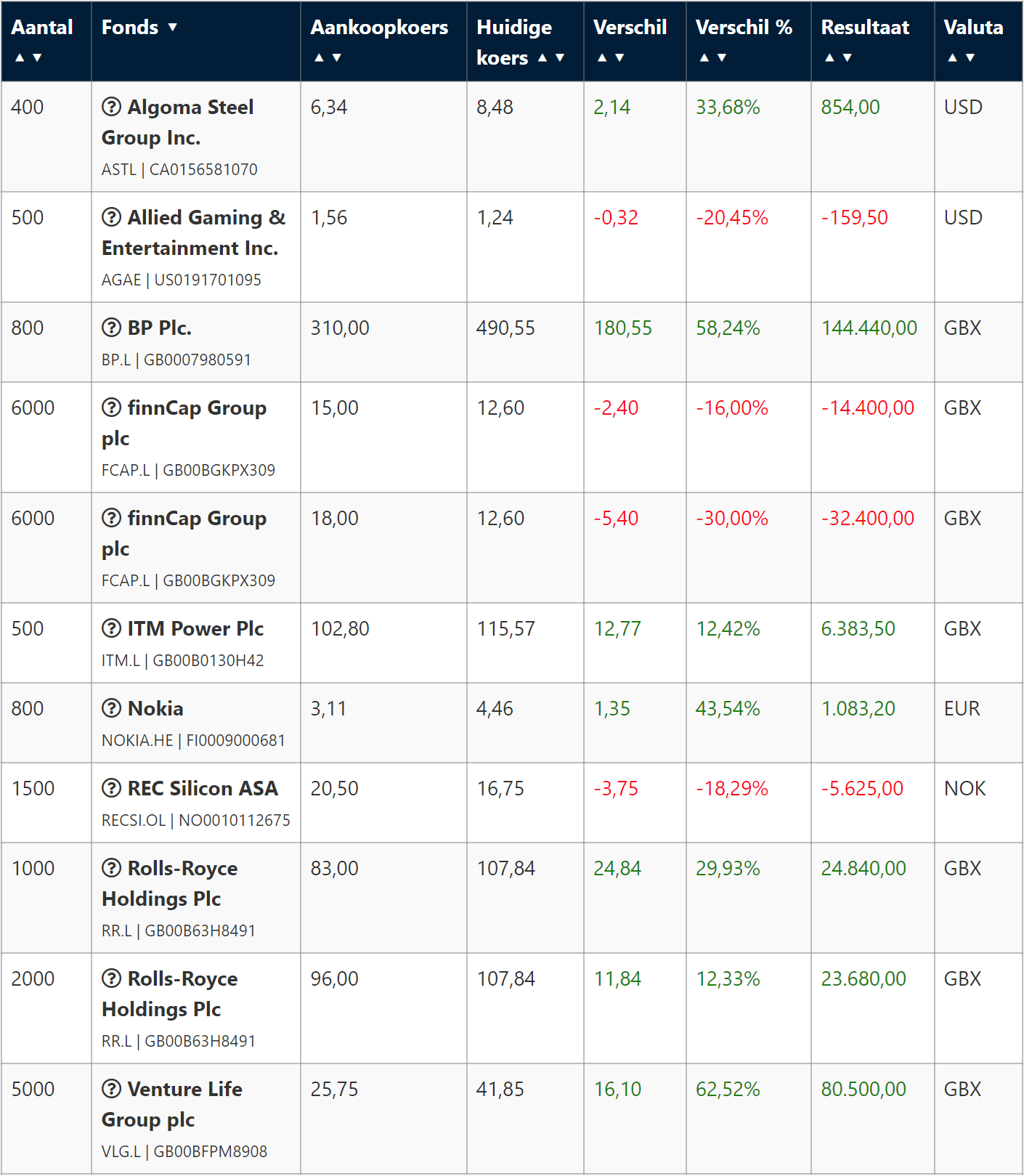

Finally, below is the portfolio overview.