The stock markets are managing to maintain their optimism. ECB members are reportedly considering raising interest rates less quickly than previously indicated, now that inflation is showing signs of falling. The expectation for the next interest rate decision remains an increase of 0.50%, as Christine Lagarde also emphasized during the last interest rate decision last December. Klaas Knot (President DNB) indicated that interest rates could be raised twice more by an interest rate increase of 0.50% and then again by 0.25%. Then we will not see any changes for a while, after which interest rate decreases can start again.

The interest rate is used as a barometer for the economy, that’s how it is! According to the Aandelenondereentientje team, investors should not cheer too soon for a milder interest rate decision as Knot claims, because the ECB has very clearly stated that they will look at how many basis points they will raise the interest rate by each meeting. They do this based on the latest macro figures that are known, of which inflation is the most important indicator. When we see Knot, we sometimes think that he likes being in the media, because what the Dutch bank thinks about it actually has little influence on the ECB’s policy.

Last week it was announced that European inflation had fallen back to an annual inflation rate of 9.2%, as expected. What was striking was that consumer prices actually fell by 0.4% and that core inflation (which is a very important figure for the ECB) actually came out higher than last month, but according to the expected 5.2%. The Americans also came through with the inflation figures, but only for products (PPI). Monthly product inflation even fell to a negative level of 0.5%, while there was still an increase of 0.2% last month. That inflation is falling is certainly a fact and very good news.

At the time of writing, the stock markets have started the new week positively, partly due to better than expected quarterly figures. As a result, fears of a recession are gradually diminishing. Our team of analysts certainly does not rule out profit-taking with a falling stock market as a result and therefore advises to keep a finger on the pulse in the coming period. We saw last week that the trees do not grow to the sky when the stock markets took a considerable step back.

Wallet

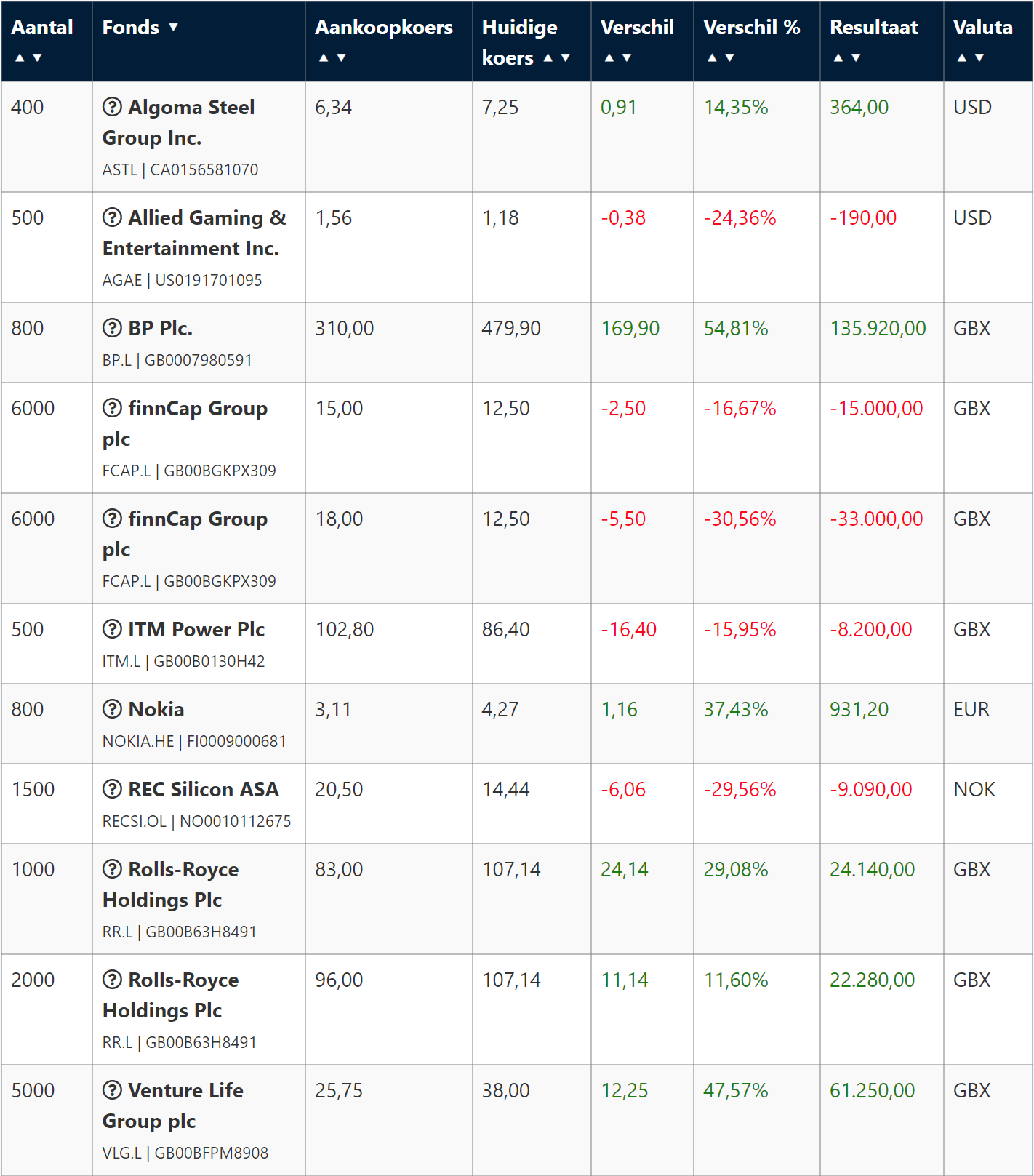

ITM Power Plc: Last week we emailed you about this speculative stock and indicated that we had taken a very small position in the stock, which was around 15% of what we normally do for a new position. The price has fallen sharply due to, among other things, the cancellation of the construction of a new factory, which was caused by increased costs and an uncertain market. As a result, management has appointed a new CEO who must implement all current and new plans that are on the table to further grow the company. Our analyst team expects that the new CEO can and must ensure improvements to keep the company on track. We therefore advise to keep volumes low, given the volatility of this stock. Management indicated in a recent trading update that they expect lower turnover and a higher EBIDTA loss, which put pressure on the price for a while. According to our analyst team, this decline offers an opportunity for the speculative investors among us.

Rolls-Royce Holdings Plc: This wonderful English company continues to make great strides and continues to amaze us with their innovative ideas. This time, news about Xanadu and Rolls-Royce . They will be working together to accelerate aerospace research, which they will do by means of quantum computing. “These are intelligent and powerful computers that process information in a new way and can thus force major and important breakthroughs. Quantum computers are expected to open doors to possibilities that are currently unthinkable.” Quantum computers are expected to play a key role in achieving the climate goals of aerospace. Rolls-Royce aims to be carbon neutral by 2050 and recently successfully tested a hydrogen-powered gas turbine in collaboration with EasyJet. We are very attached to this share and will keep it firmly in our portfolio with a longer investment horizon, because we are not going for small change with this share.

BP Plc : China seems to have the corona pandemic reasonably under control and is therefore also accelerating the reopening of the Chinese economy considerably, which could lead to a record demand of more than 101 million oil barrels per day. Due to this increasing demand, the oil price could rise again somewhat in the coming period, which could also boost inflation. Investors in BP shares are in a very good position in any case, because the price can rise considerably in the coming period, our team of analysts expects, partly due to a rising oil price.

Next Sunday, Rick van Zelst will be a guest on Business Class (RTL7) on behalf of Aandelenondereentientje. In this show, Rick will talk about the speculative hydrogen stock that you have all received by email. Finally, the portfolio overview.