CM.com reported a 6% increase in gross profit over the first three months of this year. This news caused shareholders to breathe a sigh of relief, as management proved that the disappointing figures for the fourth quarter of 2022 were not due to structural problems at the company. In addition, the company will save more costs this year than initially thought. In concrete terms, this means that an EBITDA break-even at CM.com is achievable before the end of this year.

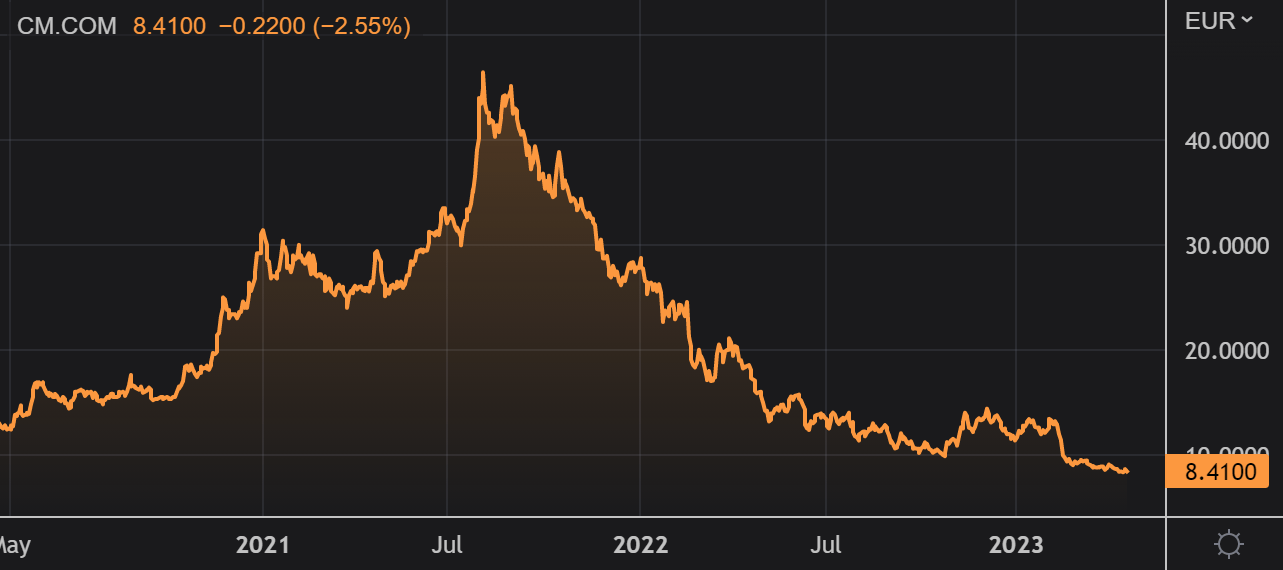

The share price has collapsed over the past 12 months. The trading update could give investors some courage, but CM.com still has a lot to prove. Analysts like the dramatic graph of CM.com, in combination with the first rays of sunshine, which is why we consider the share speculatively worth buying. We therefore buy 250 shares of CM.com at the current price of €8.41, which amounts to around 2100 euros. Although we prefer a share of a euro, this share is also well below a tenner and therefore fits our strategy. Multiples are done according to the ability to pay and the spread of your portfolio. However, it is encouraging that there now seems to be light at the end of the tunnel.

Last year was a year of bad luck

CM.com is a global leader in the cloud software sector. The company’s communication and payment platform offers its customers the opportunity to handle their trade transactions in an optimal way. Last year, the world changed for CM.com in a way that no one could have predicted. The company was one of the companies that benefited from the corona outbreak. When the end of the corona pandemic seemed to have been reached last year, many economists thought that there would be a return to normality. Instead, 2022 brought war through the Russian invasion of Ukraine, rising energy prices and rising interest rates that we have not seen in decades. Thanks to the strength and diversity of the company in terms of products, customers and markets, CM.com was nevertheless able to execute its growth plan of last year. In doing so, the company benefited from the Covid pandemic up to and including the first quarter of 2022, so the end of the pandemic was in that sense a setback for the company.

With disappointing results

For the 2022 financial year, CM.com aimed for a turnover growth of more than 30% since applying for the stock exchange listing. The money raised through the IPO could be used to further increase investments in technology and marketing. However, the end of the ‘Covid effect’ put a spanner in the works and ultimately a turnover growth of 19% was achieved. Perhaps not a bad figure, but investors had expected a little more. In response to these figures, the share price remained under pressure. All divisions showed double-digit growth in the 2022 financial year, together accounting for a record turnover of €283.2 million. ‘Ticketing’ in particular stood out with a growth of 107%. For the full year 2022, the EBITDA was €26.5 million negative (€22.3 million normalized for one-off effects). CM.com started implementing cost control measures in the course of 2022.

It is clear that 2023 is shaping up better

These efforts were continued in 2023 and with results. CM.com is currently not yet profitable, so most analysts look at revenue growth to be able to assess how quickly the underlying business is growing. In general, companies without a profit are expected to grow their revenue (significantly) every year. Management expects a further increase in revenue, but in our opinion this increase should also be accompanied by a gradual improvement in EBITDA. For the first half of this year, an EBITDA that is still three million euros negative is still expected, but by the end of this year the EBITDA should become structurally positive. An EBITDA break-even at CM.com before the end of this year therefore seems feasible.

Against this background, the analysts at Aandelenondereentientje see opportunities for this share, knowing that these are speculative opportunities. Waiting for a proven green light will certainly mean a higher purchase price, perhaps quickly above a tenner. Our objective is that we want to buy low and below a tenner and sell again as high as possible! We are therefore now buying 250 shares of CM.com in our portfolio at the current price of €8.41.

Fundamental characteristics CM.com

Name: CM.COM

ISIN code: NL0012747059

Ticker: CMCOM

Exchange: Euronext Amsterdam

Price April 20: €8.41

Highest price 52 weeks: €20.26

Lowest price 52 weeks: €8.11

Number of outstanding shares: 29,040,095

Market capitalization: 244.227 million euros

Source: Euronext