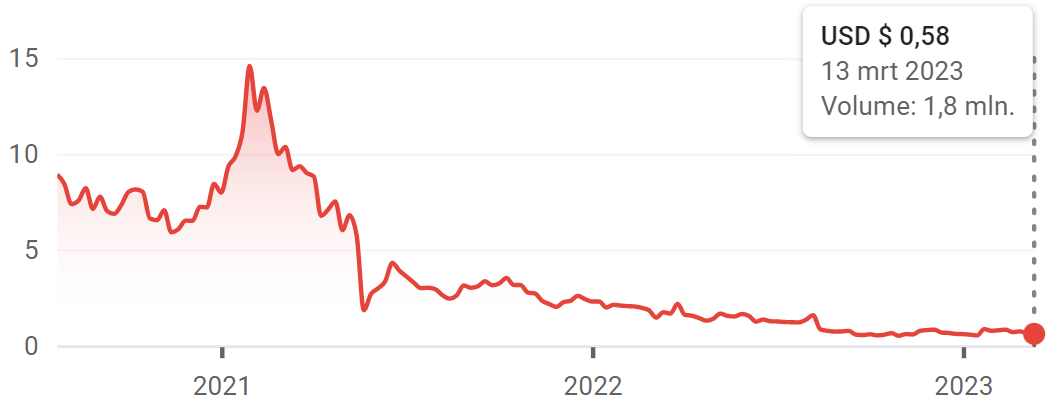

At the edge of the ravine, the most beautiful flowers bloom. In the high risk, high reward category, we found this online webshop for household appliances that made a major acquisition two years ago that went terribly wrong. Last year, several employees raised the alarm about various irregularities, which ultimately resulted in an investigation that led to the accountant withdrawing and no more financial figures being published. The results of the first investigation are now in and new management has been appointed that is open to a takeover. The price is low, which offers opportunities for investors who want to play on the scenario that the 2022 results, which will be published in a few months, do not contain any major surprises. All things considered, this share has a good chance of success, but it does have some risk. We therefore buy at half strength, which amounts to 2,500 shares at the current price of 0.58 US dollars.

1847 Gooder

In 1951, Ben Goedeker built a repair shop in his garage in St. Louis, the capital of the American state of Missouri, for televisions, which had only been on the market for a few years at the time. Due to the high demand, he soon had to open a store that also offered space to sell all kinds of electronics and household appliances. Ben passed away in 1977, after which his son Mike Goedeker took over the business and expanded it further. The company suffered greatly during the credit crisis of 2008, so Mike decided to focus on e-commerce. In 2009, Goedeker launched the website Number1direct and converted most of his showrooms into warehouses to store inventory. In 2019, he came into contact with private equity firm 1847 Holdings LLC, which subsequently acquired a dominant equity stake. The new owner changed the name to 1847 Goedeker and appointed a top executive from within its own ranks. Douglas Moore took office in August 2019 and shortly thereafter it became clear that his strategic plan was focused on an IPO.

IPO

On July 30, 2020, over 1.11 million shares of 1847 Goedeker went public at $9 each, raising over $10 million. The proceeds were used to pay down debt, strengthen working capital, and replenish cash. The former parent company, 1847 Holdings LLC, divested all of its shares in the IPO.

Major takeover

In October 2020, Moore announced its intention to acquire much larger competitor Appliances Connection. The New York-based online retailer was a good addition, particularly because it had a strong market position in the southern United States. The acquisition was completed in June 2021, after which CEO Moore was succeeded by Albert Fouerti, the former CEO and founder of Appliances Connection. He changed the name of the combined company to Polished.com.

Among the ‘pure play’ online retailers of home appliances, Polished is the largest player in the American market. The company delivers almost half a million orders annually and can generate a turnover of approximately $700 million. To finance the acquisition of Appliances Connection, 1847 Goedeker issued 91 million new shares at $2.25 each. The new shareholders also received a listed warrant per share, which gives the right to buy one share for $2.25 until June 2026.

Postponement of publication

In May 2022, CEO Fouerti presented excellent results for the first quarter of 2022, but then things went wrong. In August, only a limited update was given on the course of affairs in the second quarter, because the audit committee of the board had hired outside consultants and lawyers to conduct an investigation following complaints and allegations from employees. The news halved the share price, which had already suffered considerably from the issue that was necessary to finance the acquisition of Appliances Connection. Due to that large share issue, the price had already dropped from $15 to $2 in 2021, after which the price finally fell to a low of $0.45 in 2022 when the auditor announced that he would step down.

Abuses seem manageable

Last December, the audit committee presented the findings of the investigation. Fouerti appeared to have overbilled by approximately one million dollars and, in addition, the systems for inventory management and administration appeared to be inadequate. The board had reached an agreement with the CEO and other board members about their departure. Fouerti has deposited $3.7 million in the company’s treasury, which he also used to cover the costs of the investigation.

As a result of the inadequate inventory management, the previously reported turnover for the first quarter of 2022 has to be adjusted downwards by two million dollars. That is not pretty, but the setback will probably remain within limits because the corresponding costs will also be reduced by two million. Management does not expect to have to revise the results for 2021, while the new accountant has been given until July 31 by the stock exchange authorities to present the results for 2022.

Conclusion: good chance of takeover

Last October, Fouerti was replaced by 63-year-old Mr John Bunka. The experienced retail manager has been appointed interim CEO for six months, for which he will receive a base salary of almost $17,000 per week. If he succeeds in selling the company for an acceptable amount, he will receive a one-off bonus of over two million dollars.

Asset manager Morgan Dempsey took a 6% stake in Polished at the beginning of this year and reported in February that it had increased its stake to 7.9%. After that message, management announced that it was in constructive talks with Morgan Dempsey and that it was open to a takeover. There is interest from private parties and management has hired investment bank Jefferies as an advisor.

The valuation is difficult because few representative results have been available since the merger, but most analysts assume that the company should be able to achieve an annual turnover of at least $600 million and a profit of approximately $15 million. The profit per share would then be around $0.14. On that basis, a takeover price of $1.50 per share should be the low end of what shareholders would accept.

The team at StocksUnderOneTenty is taking a half-strength position and is buying 2,500 shares of Polished.com Inc. in the StocksUnderOneTenty portfolio at the current price of $0.58.

The author has placed a limit order for the Polished.com warrants.

Fundamentals Polished.com Inc.

Ticker: POL

ISIN code: US28252C1099

High price 52 weeks: $2.17

Low price 52 weeks: $0.42

Price at time of writing: $0.60

Number of shares: 105 million

Market capitalization: $70 million

EBITDA (2021): $48 million

EBIT (2021): $8.3 million

Net profit (2021): $7.6

Warrants Polished.com

Ticker: POL.WS

Strike price: $2.25

Expiration date: June 2, 2026

Not tradable in EU