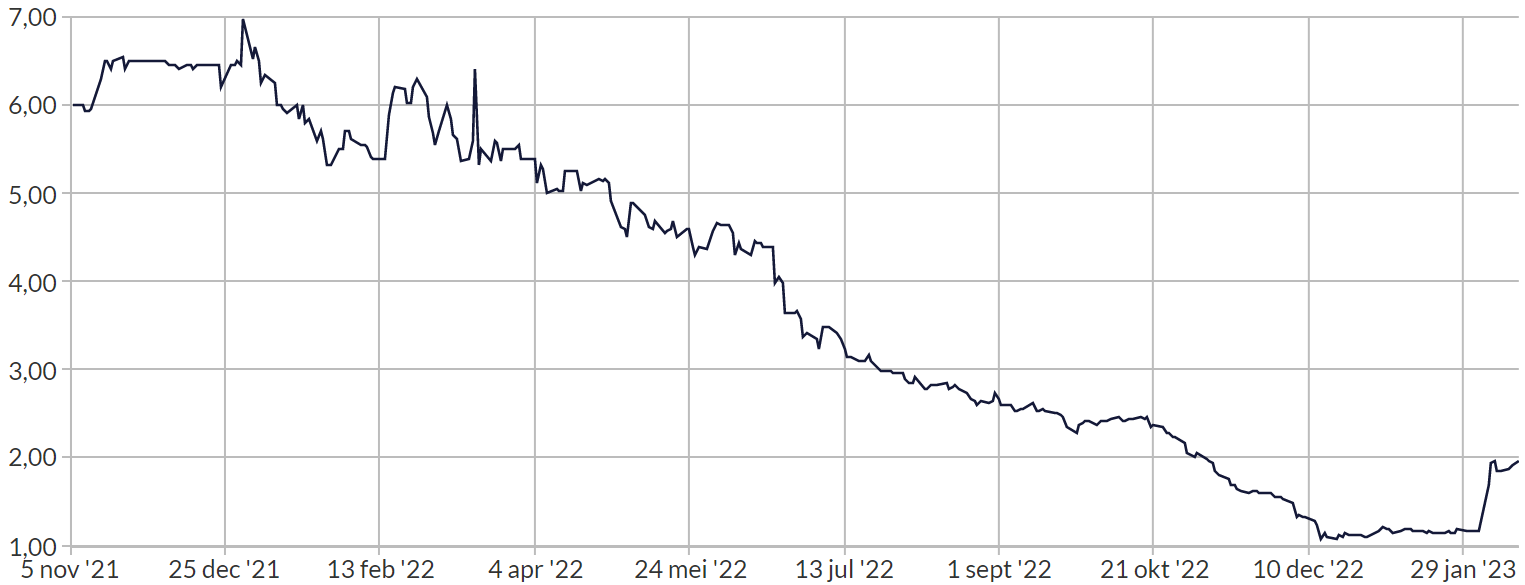

Since its introduction on Euronext Amsterdam in November 2021, MotorK has caused nothing but headaches for shareholders. The share price has fallen dramatically. The company has only been on the stock exchange for a year and for those who have the shares, it seemed as if they could write off the shares. MotorK’s business model is intact in the long term, but its exposure to the automotive sector remains a sore point. On February 23, the company will announce its figures for the 2022 financial year. In short, MotorK is a share that has gone through a deep valley with its price, but we still want to buy shares at the current price of around €1.90. We are in good company, because Luzerne, a hedge fund from the US, has now bought a 3% stake. We warn you: limit your order and do not pay the top price!

Profile

MotorK is a leading European technology company offering automotive retailers and Original Equipment Manufacturers (OEMs) an integrated Software as a Service (SaaS) platform called “SparK” to improve their digital footprint, performance and efficiency. SparK is a suite of products that supports the complete vehicle lifecycle. SparK is used to manage the digital presence of individual showroom dealers and to support the sales and marketing functions of a regional network of franchise dealers for an automotive original equipment manufacturer (OEM). Supporting services include online marketing, training and installation services.

On its website, MotorK brands itself as a leading automotive sales and marketing technology company and the only player in EMEA (Europe, Middle East and Africa) capable of delivering a full stack of products and services to support the digitalization of the entire car sales process. No other technology player in Europe has the same level of vertical expertise in the automotive industry, it states. With over 900 car dealers in Europe, MotorK offers a unique combination of SaaS products for the automotive industry. The fragmented market in which the company operates offers many opportunities for mergers and acquisitions, which has proven to be a very efficient way to acquire new customers and thus gain market share. After years of investment in R&D, sales and marketing to expand the customer base and develop the SparK platform, the next phase in the company’s evolution should be to reach the stage of profitability.

At the IPO, the company raised €75 million to finance growth by investing in product innovation, sales and marketing, but also to grow through mergers and acquisitions. The company therefore focuses mainly on the automotive retail sector in the EMEA region, with more than 400 employees and eleven offices in eight countries (Italy, Spain, France, Germany, Portugal, the United Kingdom, Belgium and Israel). MotorK is registered as a company in England, but has Italian roots. The group’s shares have been listed on the Euronext Amsterdam stock exchange since November 2021.

Numbers

The 2022 trading update was published on January 24, with results to follow on February 23. This Q4 and full-year trading update was MotorK’s best-ever quarter in the company’s history, with a robust pipeline paving the way for further growth. The company reported annual recurring revenue (ARR) of €5.1 million in Q4, up 25% from Q3. Full-year ARR was €26.9 million, including €9.7 million from M&A, compared to €15.1 million in the prior year (€2.7 million from M&A), or an organic increase of 40% and an increase of 78% including M&A. However, 2022 ARR was slightly below the expected range of €28-30 million. In the explanation of the figures, management emphasized the success of the strategic initiatives that the group had launched during the year, in particular the focus on the Enterprise segment, the contribution of the recently acquired companies and the commercial launch of the SparK platform. Now we are looking forward to the annual figures that will be announced on February 23. The moment of truth!

Pros:

- News of big interesting deals can give the price a boost.

- Sufficient opportunities for mergers and acquisitions to accelerate growth.

- New product development or updates can improve the SparK platform.

Cons:

- Not all mergers and acquisitions have a chance of success.

- The automotive sector is cyclical in nature and this can weigh on results.

- Risks of balance sheet deterioration remain if profitability does not improve quickly.

Conclusion

Let’s not beat around the bush: the performance of MotorK shares on the stock exchange has been very disappointing so far. The software company had difficulty attracting investors from the start and was therefore forced to postpone the IPO several times and to lower the bandwidth of the introduction price to €6.50, which was significantly lower than what had been hoped for. That was where the misery began for the shareholder. The price has suffered a long time since the IPO almost a year and a half ago and has fallen to €1.10.

The question is of course whether improvement can be expected. The company is still in a growth phase, in which we can expect more acquisitions in the coming months and years. Investors did not seem prepared to wait until MotorK has outgrown the pioneering phase and has become profitable. A number of factors play a role in this that the company itself has no control over. We are thinking, for example, of the stock market’s decreased appetite for technology shares last year. It was clear that the time is over when a company with an interesting technology automatically ended up on the list of favorite shares of many investors. In addition, the focus on the automotive sector also weighs on the price. This sector is struggling with many uncertainties. For example, it is certainly unclear who will emerge as the winner in the electric car market. The future of self-driving cars, which has become remarkably quiet at the moment, also remains uncertain. These markets will all be able to contribute to the growth of MotorK.

On the other hand, there are also strong points of MotorK that we should not overlook. The current valuation looks attractive according to some analysts at a valuation level of less than 2x EV/revenue. Such a level has historically proven to be an attractive entry point for SaaS (Software-as-a-Service) companies. MotorK has shown rapid revenue growth in the past and looking at the coming years, the company has the potential to become one of the fastest growing smaller B2B SaaS companies in Europe. One should also take into account the potential pipeline of acquisitions that management is focused on. Successful acquisitions could accelerate growth, with growth potentially twice as fast as its main competitors in a best case scenario.

We attribute the current significant discount at which MotorK is listed compared to its peers mainly to the limited track record and the low liquidity of its shares. In addition, we would also like to see evidence that profitability can be achieved in the relatively short term. In short, there are many positive aspects to MotorK. The publication of the annual figures on 23 February will determine the direction of the share. After the strong correction in the price, we want to enter in a limited way. We normally buy within our Shares Under a Tenner portfolio for around €3000 per share. But now we are cautiously buying 1000 shares of MotorK, so for around €1900 based on a price of around €1.90. If the figures on 23 February are good, we can always see what we do next. Shares Under a Tenner gives the shares an initial price target of €2.75. Limit your orders!

Fundamental characteristics MotorK

Earnings per share 2022: –

Tax. earnings per share 2023: € 0.04

Tax. earnings per share 2024: € 0.14

Price-earnings ratio 2022: –

Price at time of writing: € 1.87

ISIN code: GB00BMXH3352

Ticker symbol: MTRK.AS

Price high last 12 months: € 6.42

Price low last 12 months: € 1.09

Dividend: –

Dividend yield: –

Number of outstanding shares: 39.21 million

Market capitalization: € 73.31 million

Sector: technology

Return on assets: -15.84%

Return on equity: -89.17%