In our search for undervalued shares under ten euros, we found the American Sunlink Health Systems in the healthcare sector. The small company from Atlanta in the southern state of Georgia is listed far below its tangible book value of $2.33 per share. There is a lot of hidden value in the balance sheet due to the way in which the real estate, the pharmacy chain and the deductible losses are valued. With the price at the time of writing of $0.84, we are buying a dollar for 36 dollar cents, so to speak.

The team at Aandelenondereentientje also had its eye on the share in 2020. The price was then listed at $1.20 and we gave it a price target of at least $1.92 and possibly $3.00. After the initial decline as a result of the coronavirus, both price targets were nevertheless reached within twelve months. Now, almost three years later, the price has fallen so far that we are including 3000 shares of Sunlink Health Systems in the Aandelenondereentientje portfolio.

The company

Please note: the financial years are broken and run from July 1 to June 30.

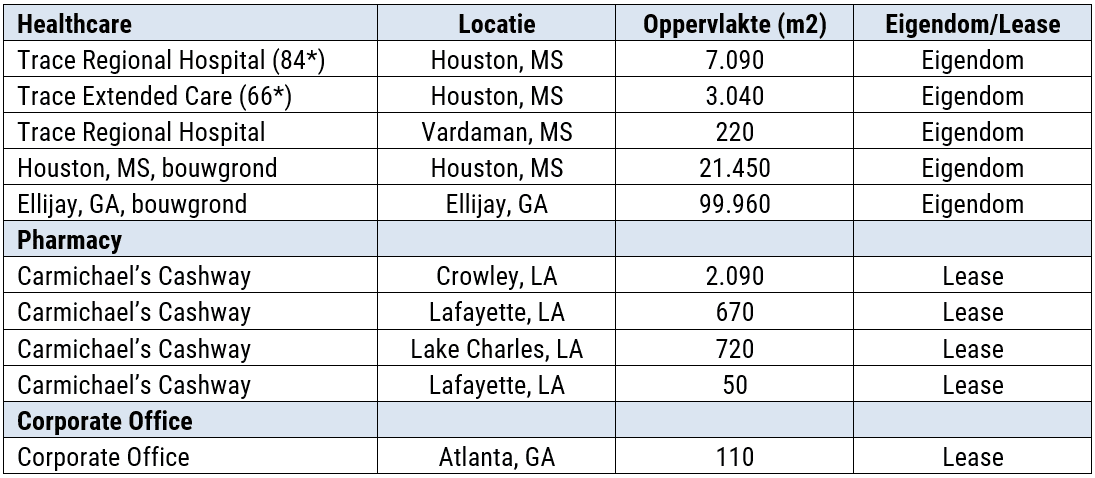

Sunlink operates an 84-bed hospital, a 66-bed nursing home and a small subsidiary in Mississippi. In neighboring Louisiana, it operates four pharmacies under the Carmichael’s Cashway brand. Sunlink owns the hospitals and leases the pharmacies. The company also owns significant tracts of land in Houston, Mississippi and Ellijay, Georgia.

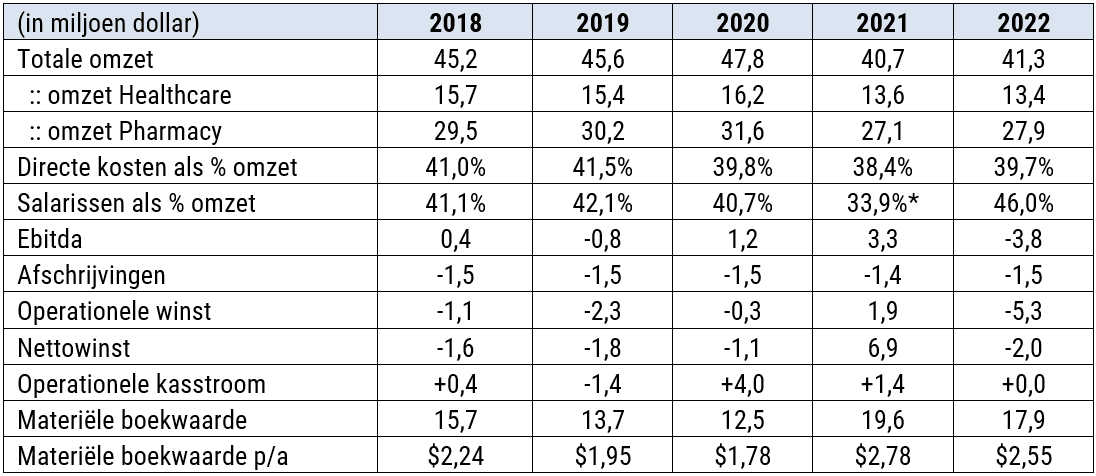

In the broken financial year 2022, 68% of the turnover came from the pharmacy chain and 32% from the operation of hospitals. Table 2 shows the turnover and profit development over the past five years. The operating result was often negative, although the operating cash flow fortunately often remained positive. Although the coronavirus initially had a negative impact on turnover, Sunlink subsequently benefited fully from government regulations that allowed it to reduce costs and boost its cash position. The financial year 2021 even ended with a net profit of $6.9 million. In 2022, however, the operating profit was negative again due to the sharp increase in wage costs. Where normally less than 42% of turnover was spent on wage costs, that percentage rose to 46% last year. Since a wage cut is not a realistic option, management must increase rates.

Development of the quarterly figures

Table 3 shows that wage costs have recently increased to over 48% of turnover. EBITDA threatens to remain negative and drag down the operational cash flow. Management is now doing everything it can to pass on the rates of the increased wage costs to customers. In the coming period, investors will have to monitor closely to what extent this will be successful.

The financial position

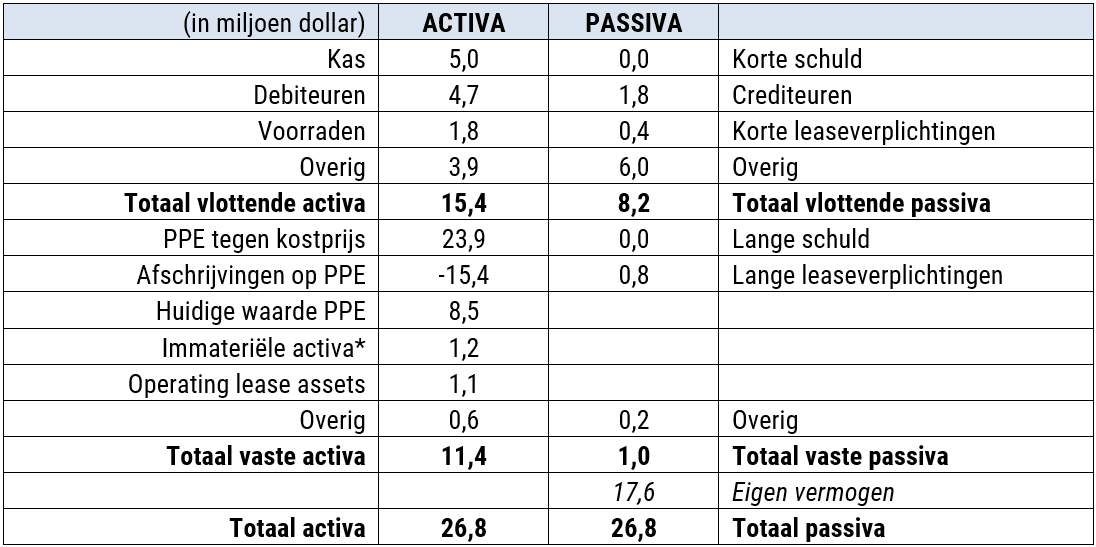

Table 4 shows that there is $5.0 million in cash and debts are zero. We calculate the tangible book value by reducing the equity of $17.6 million by the $1.2 million in intangible assets. The resulting $16.4 million converts to $2.33 per share.

Hidden value

The tangible book value of $2.33 per share is an absolute floor for the valuation. After all, there is a lot of hidden value in the balance sheet due to the way the real estate, the pharmacy chain and the deductible losses are valued:

- The balance sheet item PPE consists almost entirely of real estate that is booked at cost price minus cumulative depreciation for $8.5 million. However, these depreciations are purely fiscally driven, as real estate increases in value in practice. The lion’s share was purchased in 2001 and now most likely has a higher sales value. Even in a conservative scenario based on cost price, the value of the real estate amounts to $23.9 million instead of the $8.5 million stated on the balance sheet. The tangible book value may therefore be estimated $15.4 million higher.

- De apotheekketen is voor slechts $1,2 miljoen ondergebracht in de balanspost immateriële activa. Dat is niet reëel omdat deze keten een jaaromzet heeft van bijna $30 miljoen en daarop een ebitda-marge behaalt van gemiddeld zo’n 5% (zie tabel 5). Een reële EV/ebitda multiple zal minimaal op 4x liggen, waarmee de ondergrens voor de waarde van de apotheekketen uitkomt op $6,0 miljoen in plaats van de ingeboekte $1,2 miljoen. De reële materiële boekwaarde is dus $4,8 miljoen hoger.

- Sunlink heeft voor $23,1 miljoen aan compensabele verliezen opgebouwd, die opgevoerd mogen worden tussen 2023 en 2038. Een overnemende partij kan daarmee een aanzienlijk belastingvoordeel behalen. Aangezien de uiteindelijke realisatie van compensabele verliezen onzeker is, laten we de waarde voorzichtigheidshalve buiten beschouwing.

De onderwaardering van het vastgoed en van de apotheekketen bedraagt opgeteld minimaal $20,2 miljoen. Onderliggend komt de reële nettovermogenswaarde dan uit op $36,6 miljoen, oftewel $5,20 per aandeel, wat aanzienlijk hoger is dan de $2,33 van de balans.

Conclusie: koopwaardig op koersen tussen $0,80 en $1,00

Met de huidige koersen is een overname van Sunlink sowieso een reële mogelijkheid. Een overnemende partij kan de verborgen waarde vrijspelen en zou door schaalvergroting ook de winstgevendheid substantieel kunnen verbeteren. In het algemeen zit het grootste gevaar voor de aandeelhouders van matig renderende, maar ondergewaardeerde bedrijven in het ‘agency-dilemma’. Het management wordt dan zodanig royaal vergoed dat het geen belang heeft bij een overname. Bij Sunlink zijn de salarissen en vergoedingen echter laag, zodat die belangenconflicten niet spelen. Sterker nog, het management blijkt zelf bijna 30% van de aandelen te bezitten.

De reële nettovermogenswaarde ligt tussen de $2,33 en $5,20 per aandeel, en dan zijn de compensabele verliezen nog niet eens meegerekend. We geven Sunlink Health Systems een koopadvies met als voorlopig koersdoel $2,35, wat de absolute ondergrens is van de reële nettovermogenswaarde. Met een beurswaarde van $6 miljoen behoort Sunlink tot de categorie micro- of nanocaps die inherent risicovol zijn.

Beleggers dienen voorzichtig te werk te gaan, hun posities beperkt te houden en vanwege de beperkte verhandelbaarheid alleen limietorders in te leggen. Aandelenondereentientje koopt voorzichtig 3000 aandelen Sunlink in de portefeuille.

De auteur bezit aandelen Sunlink Health Systems.

Belangrijke aandeelhouders

Steven Baileys (director): 11,8%

Robert Thornton (CEO): 8,0%

Wittenberg Investment Management: 7,5%

Wellington Management: 4,4%

Renaissance Technologies: 4,1%

Acadian Asset Management: 3,6%

Howard Turner (director): 3,3%

Bridgeway Capital Management: 3,3%

Millennium Management: 3,3%

Kennedy Capital Management: 2,1%

Key Facts Sunlink Health Systems

Name: Sunlink Health Systems Inc

Ticker: SSY

Exchange: AMEX

ISIN: US86737U1025

Price at time of writing: $0.84

52-week low: $0.53

52-week high: $2.10

Number of shares outstanding: 7.04 million

Market capitalization: $5.9 million

Cash position: $5.0 million

Total debt: $0.0 million

Net assets: $5.0 million

Enterprise value (EV): $0.9 million

Tangible book value: $16.4 million

Tangible book value per share: $2.33

Price/tangible book value: 0.36x

Dividend per share: $0.00