Aegon’s share price has fallen to €3.95, a level we previously only dreamed of. Investors are uncertain about the exposure to investments in the banking sector and in particular Credit Suisse. Well, that is completely out of the question, according to our calculations at Aandelenondereentientje. According to analyst calculations, the group owns a total of €3 million of Credit Suisse AT1 bonds. Whether the insurer also participated in the share capital of the Swiss bank is unknown. In contrast to other weak banks, Aegon only has €20 million of these types of loans. So this is not worth mentioning!

The price is now just under €3.95. We strike and buy 1000 shares in the portfolio of Aandelenondereentientje. The most important step is the divestment of the Dutch insurance activities that were sold to ASR. This will yield billions and also 30% of the ASR shares. Investors are being spoiled with a high dividend of €0.30, which is almost 7.5% at the current price! Investors seem to have no patience, too bad for them and good for us.

Is rising interest rates a concern?

Interest rates are the most important factor for the results of both insurers and banks. For insurers and pension funds, higher rates for long-term interest rates are favourable. After all, higher interest rates ensure better returns on loan portfolios. On the other hand, long-term interest rates are also indicative of the value of liabilities. At higher interest rates, discount rates increase, which reduces the net present value of future payments. For banks, on the other hand, it is not so much the long-term interest rate that is important, but the interest rate term structure (yield curve). After all, banks borrow at rates for short-term loans and lend out business loans and mortgages at long-term rates. For banks, an upward-facing yield curve with low short-term interest rates and high long-term interest rates is therefore favourable, while a so-called inverse yield curve with high short-term interest rates and low long-term interest rates is very unfavourable.

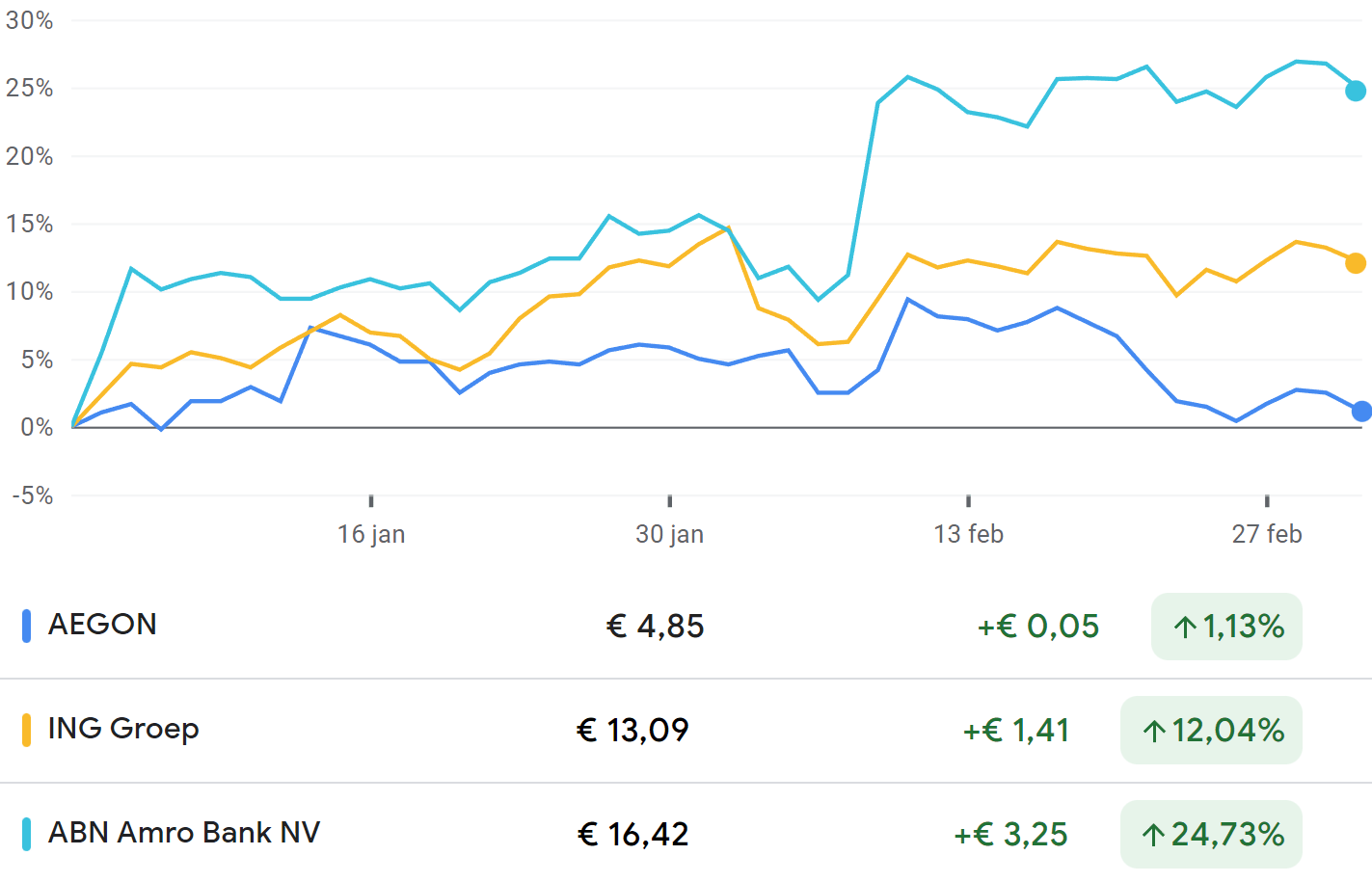

Interest rates have risen across the entire yield curve in 2022, but short-term interest rates have risen faster, which has caused the yield curve to become the opposite since September. The interest rate structure of the past quarters has therefore been extremely unfavourable for banks, while the high long-term interest rate is now favourable for insurers. Nevertheless, we saw exactly the opposite on the stock exchange earlier this year among Dutch financials. ABN Amro had risen by 24%, ING almost 11%, while Aegon had done nothing. Now that bank shares are falling due to the problems within the sector, it appears that Aegon is getting an extra headbutt, a drop of 20%. No matter how we search and analyse: no one has a good explanation for that. Investing can sometimes be elusive, but we seize our chance.

Great confidence in the new CEO

Aegon was originally created as a result of the merger between Ago and Ennia. Since the merger in the eighties, the company has grown rapidly by making acquisitions in various countries. Now, in the aftermath of the credit crisis, some divestments had already taken place, but the group was still an inefficient insurance conglomerate with a decentralized organizational structure consisting of a wide range of local insurance companies that were relatively independent. In 2020, the current CEO, Lard Friese, took office with the clear mission to bring more focus because margins and profitability must increase.

Sell part and focus on what remains

In 2020, Aegon announced that its Central and Eastern European activities would be divested for €830 million, which was completed in June 2021. This was followed last November by the announcement of a much larger divestment, namely the Dutch activities. ASR is buying the Dutch activities for €2.2 billion in cash, while Aegon will also receive a 30% equity stake in ASR. In total, the acquisition had a value of €4.9 billion.

Once the acquisition is completed in June, Aegon will use 1.5 billion euros of the proceeds for the benefit of its shareholders. A large part of this will probably take the form of a one-off bonus dividend. The remaining €700 million will be used to reduce the debt position of €5.6 billion at holding level. Incidentally, the holding’s cash position is well-stocked with €1.6 billion in liquid assets. The dividend for the 2022 financial year will be 24 cents and will be increased to 30 cents in 2023.

The knife cuts both ways. ASR will use the economies of scale to increase returns, while Aegon strengthens its capital position and can focus better on its largest market, America. The American activities not only include the activities in the United States, but also those in Canada and Brazil. There are three interesting divisions: collective pension plans, individual life insurance and health insurance.

A significant portion of the turnover comes from the division of collective pension plans, which provides pensions for 3.6 million employees of the affiliated companies and organizations. The division has over $200 billion in management, for which it charges management and administration fees. Management is very positive about the division, but so far growth is too low. The number of insured has even been declining for several years.

Aegon provides life insurance to individuals, which is also often offered through employers. This division normally delivers an operating result of just under $300 million, although last year it was only $190 million due to the payments to the survivors of the victims of the mysterious excess mortality that has also occurred in America since 2021. The result will improve in the coming quarters because the excess mortality will ebb away and because of the higher interest rates, but it will also be a major challenge for this division to grow structurally.

Aegon provides policies for people who are looking for additional coverage for their healthcare needs. The results of this division benefited last year from the excess mortality, because healthcare costs for the deceased disappeared. However, these activities are structurally shrinking, which means that the return is too low. The division is a kind of cash cow that will continue to contribute to the group result for the time being, but the management will not make any major investments.

Numbers were fine despite being red

The fourth quarter of 2022 resulted in a net loss of €2.5 billion. However, the mega loss was mainly accounting in nature, as it included a large book loss related to the sale of the Dutch activities that had been sold below balance sheet value. According to analysts, the underlying operating result for the fourth quarter of €488 was above expectations. The CEO was pleased with the progress in streamlining the organization. A previously initiated savings program that should reduce annual costs by €400 million has already been largely realized and margins can increase.

We buy 1000 shares

After the sale of the Dutch activities, management has its hands free to concentrate on the remaining activities that clearly require attention. After all, the American portfolio has potential, but is no longer growing.

The important indicator for the state of affairs is the free cash flow that can be transferred annually from the business units to the holding company, from which the dividend is then paid. Last year, this free cash flow amounted to around €600 million and is expected to increase to €800 million within two years. With an enterprise value of around €13 billion, the return (FCF yield) then amounts to 6%. The dividend yield was also 6% and the share was listed at 70% of its book value until recently. By all standards, the share is therefore definitely not expensive. The prospects are relatively favourable, because the result will increase due to the efficiency improvements and especially because the interest rate has risen, which is why we are buying 1000 Aegon shares in the portfolio of Aandelenondereentientje.

Fundamental data Aegon

Ticker: AGN

ISIN code: NL0000303709

Closing price March 23: € 3.94

Lowest price 52 weeks: € 3.59

Highest price 52 weeks: € 5.42