Let’s be honest — it does look good when you’re trading “shares under ten” and you’ve got Rolls-Royce in your portfolio. Despite the prestigious name, this stock fully qualifies as a true penny stock. Shares Under Ten is adding 2,000 shares to the portfolio at the current price of around 97 pence.

Company Profile

The Rolls-Royce brand is, of course, best known for its luxury cars — but many may not realise that the automotive business has long been owned by BMW. Rolls-Royce Holdings plc, founded in 1884 and headquartered in London, operates independently and focuses on engineering and power systems.

The company is structured into four divisions: Civil Aerospace, Power Systems, Defence, and New Markets.

- The Civil Aerospace division designs, manufactures, and services engines for large commercial aircraft, regional jets, and business aviation.

- The Power Systems division develops and sells integrated power and propulsion solutions for marine, defence, and selected industrial sectors.

- The Defence division supplies engines for military transport aircraft, patrol aircraft, and naval propulsion.

- The New Markets division focuses on small modular reactors (SMRs) and new electric energy solutions, as well as maintenance, repair, and overhaul (MRO) services.

The New Markets division is expected to play a key role in the global energy transition. Rolls-Royce is working to accelerate the launch of a new generation of mini nuclear reactors, a development fast-tracked by the ongoing energy crisis. While these SMRs aren’t expected to be operational before the early 2030s, management is eager to speed up the process, especially as Western nations seek to reduce dependence on Russian fossil fuels following the invasion of Ukraine.

However, engineers within the company have expressed frustration with the slow pace of regulatory approval in the UK, arguing that the government’s process for reviewing reactor safety is unnecessarily burdensome. Rolls-Royce aims to build SMRs that generate around 470 megawatts of power — just one-seventh the output of a large-scale nuclear plant, but at roughly one-twelfth the cost. The UK government has stated that the company’s technology is entirely new and must therefore undergo thorough scrutiny. Rolls-Royce engineers, however, point out that the technology is based on decades of experience in nuclear-powered submarines, a proven and extensively tested field.

Rolls-Royce cannot be acquired without government approval. The UK government holds a so-called “golden share,” which grants it special veto rights. This share does not offer profit participation or capital rights, but allows government representatives to attend general meetings and block specific strategic moves — such as takeover bids — that could affect national interests.

Financials

The UK’s most well-known engineering firm was hit hard by the COVID-19 pandemic, as airlines pay Rolls-Royce based on the number of flight hours logged by its engines. Given these extraordinary circumstances, FY2020 and FY2021 are not considered reliable indicators of the company’s underlying performance. In 2021, Rolls-Royce reported £414 million in underlying operating profit, a sharp turnaround from a loss the previous year. Growth in the Power Systems and Defence divisions contributed significantly to this financial improvement. However, the company also reported a free cash outflow of £1.5 billion from continuing operations in the same year.

CEO Warren East commented on the results:

“We have improved our financial performance, met our short-term commitments, secured new business, and made important strategic progress during the year. While challenges remain, we are increasingly confident about the future and the significant commercial opportunities presented by the energy transition.”

Rolls-Royce’s credit profile has improved since the onset of the pandemic, and its exposure to the Russia-Ukraine conflict remains limited. As a result, Moody’s upgraded the company’s outlook from negative to stable.

Pros

- Strong visibility and predictability of earnings

- Stable margins in the Defence division

- New CEO Warren East is aiming to bring fresh momentum to the company

Cons

- Loss of market share in the business jet segment

- Disappointing cash flow development

- High R&D costs for new engine programmes

Conclusion

We are not particularly enthusiastic about this stock. While management certainly shows no lack of ambition, those good intentions have yet to translate into improved results. The company appears to be spread too thin across too many markets — and it’s simply not possible to be best-in-class everywhere. A more focused approach would likely serve Rolls-Royce well. Divesting non-core activities and doubling down on key strengths could strengthen both performance and investor confidence. The business jet division, for example, already faced structural challenges before the energy crisis, and its outlook remains weak. A sale of this unit might be a sensible move — especially if a solid price can still be secured. Back in August 2021, management announced it was open to selling assets such as ITP Aero, the turbine blade manufacturer, in an effort to raise at least £2 billion. Strategic asset sales like these may be necessary to unlock value and refocus the company.

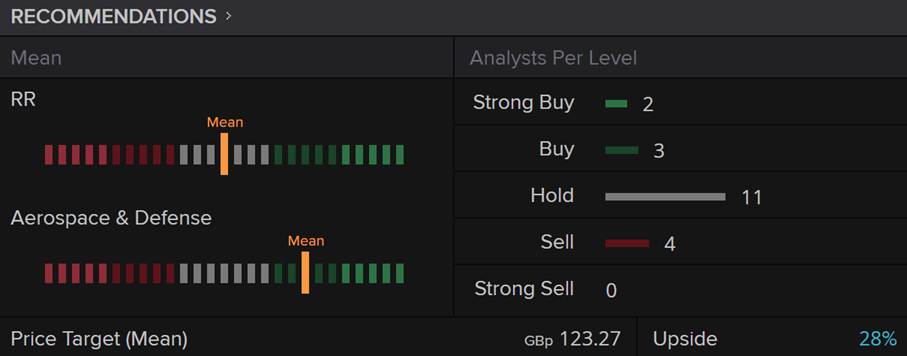

Third-Party Analyst Ratings for Rolls-Royce.

Globally, twenty analysts currently cover Rolls-Royce Holdings, and the consensus view is that the stock could gain around 28% over the next 12 to 18 months. At Shares Under Ten, we believe the share price has likely found a bottom, and we’re taking this opportunity to add the stock to our portfolio. Naturally, we’ll be monitoring developments closely. A takeover seems highly unlikely under current circumstances. Rolls-Royce plays a vital role in the UK defence sector, and the government holds a golden share that gives it veto power over any unwanted acquisition. In addition, ceding control over Rolls-Royce’s expertise in modular nuclear reactors would run counter to the UK’s long-term energy policy. Former Prime Minister Boris Johnson has been a strong advocate for nuclear energy and clearly sees the company’s know-how as a strategic national asset — especially amid the current energy crisis.Takeover rumours have surfaced before. Rolls-Royce was the subject of M&A speculation both in 2015 and again in 2020. However, following a series of profit warnings in 2015, the stock price fell by around 75%, and its recovery since then has been, to put it mildly, slow and inconsistent.

We would also like to highlight that in the most recent financial year, 31% of Rolls-Royce’s revenues came from its Defence division. Meanwhile, we remain positive on the long-term potential of the company’s New Markets segment, particularly in the area of small modular reactors (SMRs). While this business won’t contribute meaningfully to earnings in the short term, we see substantial growth potential further down the line. In our view, CEO Warren East is doing everything in his power to guide Rolls-Royce back to long-term success. The one-year share price chart shows sharp rallies at several points, but with the stock having pulled back 10% in recent weeks, we are taking advantage of the dip and are adding 2,000 Rolls-Royce shares to the Shares Under Ten portfolio.

Key Fundamentals – Rolls-Royce Holdings plc

- ISIN Code: GB00B63H8491

- Ticker Symbol:L

- Exchange: London Stock Exchange

- Earnings Per Share (2021): £0.12

- Taxed EPS (2021): £0.62

- Taxed EPS (2022): £4.62

- P/E Ratio (2020): 8

- Share Price Used:37 pence

- 52-Week High:91 pence

- 52-Week Low:49 pence

- Dividend: –

- Dividend Yield: –

- Shares Outstanding:37 billion

- Market Capitalisation: £8.32 billion

- Sector: Technology

- Return on Assets: 1%

- Return on Equity: –