Last year, SharesUnderTen scored big with this stock. We issued a Buy recommendation when the price was between €5 and €6. The stock rallied almost immediately, hitting our price target of €13 before the year was out. We exited a bit earlier, but investors who held on locked in gains of over 135% in just six months. Since then, the price has pulled back to below €8. But despite the drop, the recently released annual results were anything but disappointing. While revenue came in slightly below expectations, profitability beat estimates. More importantly, management shared a positive outlook for 2025. Cautiously optimistic in a choppy market, we’re adding 150 shares back into our SharesUnderTen portfolio. Not a bold bet—just a smart, calculated move with solid upside potential.

Company Profile

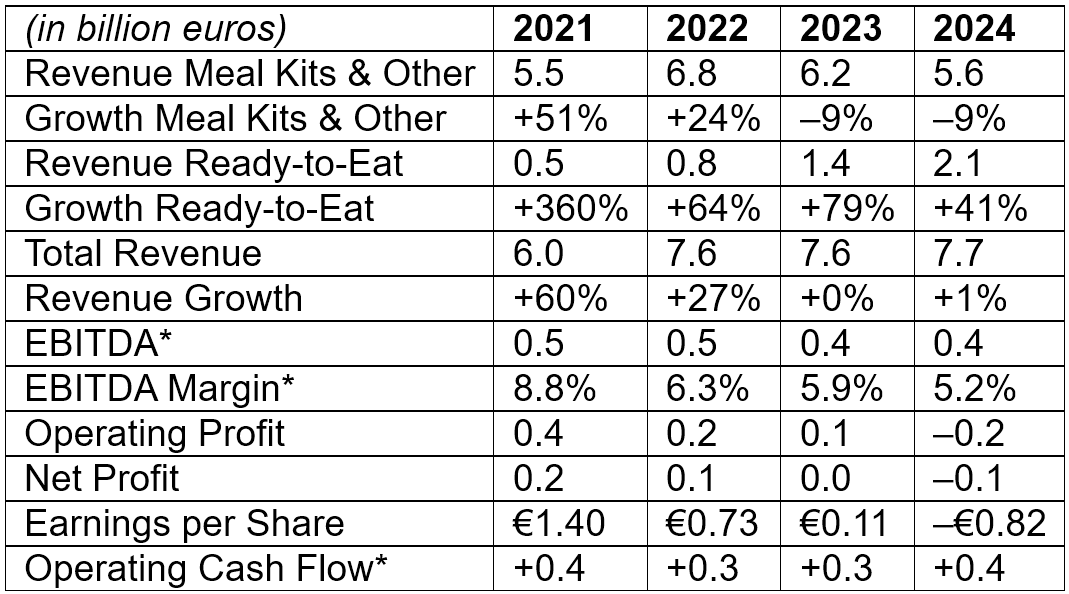

Founded in 2011, HelloFresh is one of the standout success stories to emerge from startup incubator Rocket Internet. The company went public in 2017 at €10.25 per share. Rocket Internet gradually reduced its stake after the IPO and fully exited in 2019, selling its remaining shares at around €8 each. In hindsight, not the best timing—since the stock went on a massive rally, peaking near €100 in 2021. Since then, however, the share price has dropped sharply as revenue growth has stalled (see Table 1). That’s not entirely surprising: with an estimated 50% market share, HelloFresh is running up against the natural limits of its core business. That’s not necessarily a bad thing—as long as profitability can be improved.

And that’s exactly where management is now focused, launching several cost-cutting initiatives to boost margins.

HelloFresh operates two divisions: Meal Kits and Ready-to-Eat.

- The Meal Kits division includes the original business: the well-known boxes with fresh ingredients that customers cook themselves.

- The Ready-to-Eat division is a newer and rapidly growing segment: pre-prepared meal solutions that require no cooking.

Ready-to-Eat is currently growing at a rapid pace and already accounts for more than a quarter of total revenue. The expectation now is that the decline in the Meal Kits segment will stabilize, while the Ready-to-Eat segment continues to expand. In short: HelloFresh still has plenty of room for growth—just from a different direction than before.

Table 1: Results over the past 4 years. *Adjusted for one-off items

Table 1: Results over the past 4 years. *Adjusted for one-off items

Outlook

At the release of its annual results on 11 March, management announced that, thanks to ongoing cost-saving measures, normalized operating profit is expected to rise by over 65% in 2025, reaching €225 million. Normalized EBITDA is projected to come in at €475 million. However, the company also noted that a number of one-off expenses will be incurred due to restructuring efforts and investments aimed at improving operational efficiency.

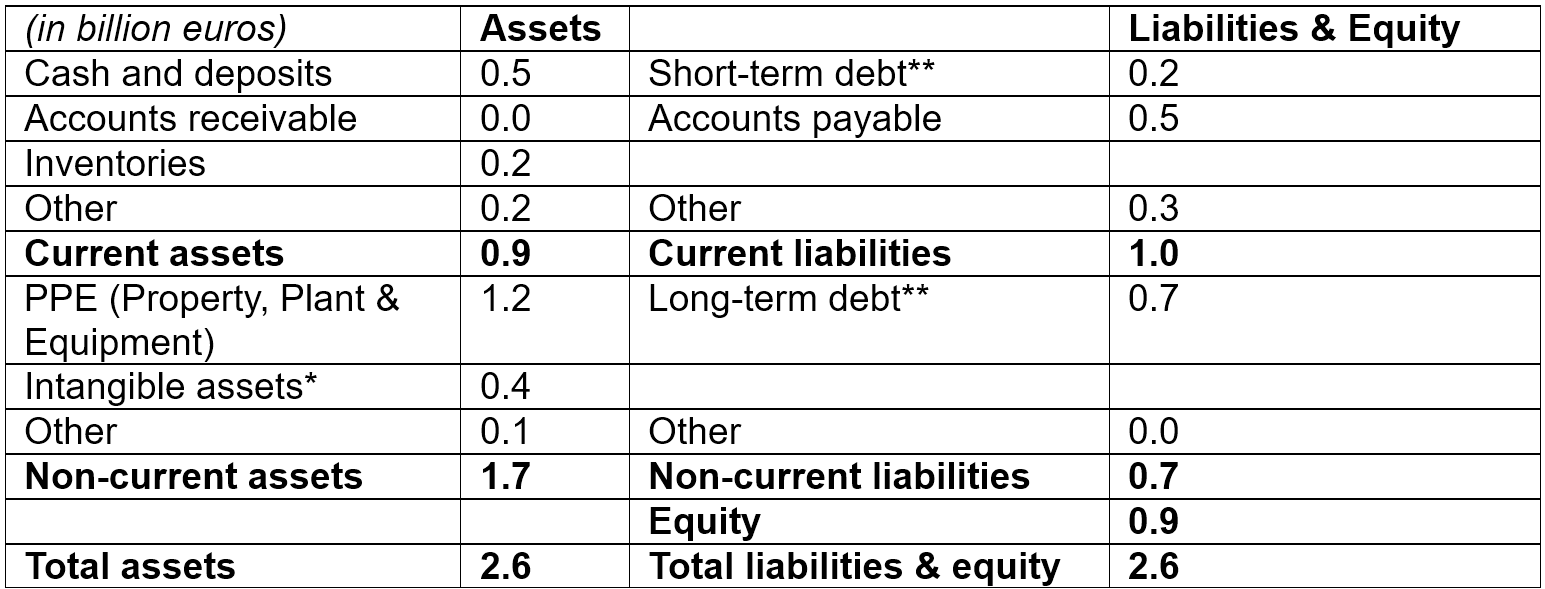

Table 2: Balance Sheet as of December 2024. *Including goodwill. **Including lease liabilities.

Table 2: Balance Sheet as of December 2024. *Including goodwill. **Including lease liabilities.

Table 2 shows that intangible assets are valued at €0.4 billion. This implies that roughly €0.5 billion of tangible book value remains within equity, or €2.96 per share. Total debt amounts to €0.9 billion, while cash and cash equivalents stand at €0.5 billion. This results in a net debt position of €0.4 billion. Based on normalized 2024 EBITDA, the net debt/EBITDA ratio is just 1.1x. This means HelloFresh is far from its maximum borrowing capacity and can easily raise additional liquidity if needed.

CEO Increases His Stake

In September, it was announced that co-founder and CEO Dominik Richter privately purchased 1.5 million shares for a total of approximately €10 million. As a result, his ownership stake increased from 4.2% to 5.0%. We view this as a very strong signal—the ultimate insider showing confidence by making a personal, high-conviction investment of this scale.

Share Buyback Program

Throughout 2024, HelloFresh repurchased approximately 10.3 million shares under its share buyback program, at an average price of €8.00. Although the program was originally set to expire in December, it has been extended, with an additional €75 million allocated for further repurchases in 2025. At the current share price, this allows for the repurchase of 9 to 10 million shares, representing more than 5% of total shares outstanding. Given the depressed share price, we believe this is a highly effective use of capital.

Valuation Forecast

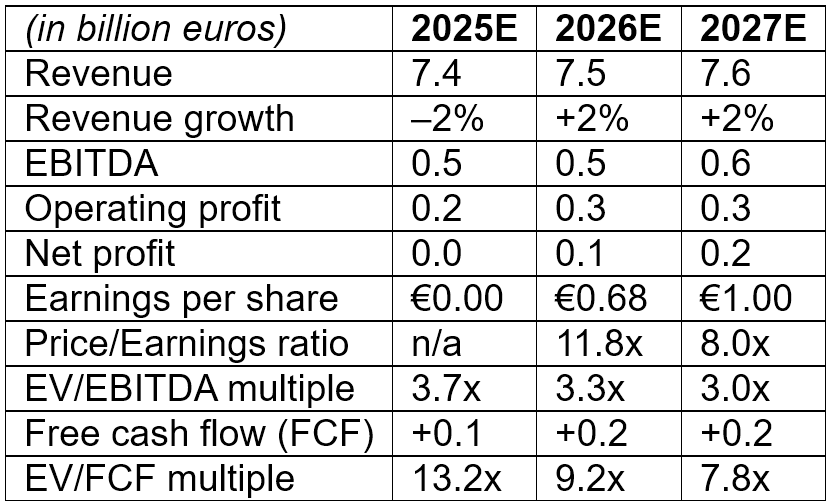

As shown in Table 3, based on 2027 estimates, HelloFresh is trading at a price/earnings ratio of 8.0x and an EV/FCF multiple of 7.8x.

Table 3: Estimates through 2027

Table 3: Estimates through 2027

Conclusion: Worth Buying

The valuation metrics just mentioned are suspiciously low for a market leader. That said, we’re confident there are no skeletons in the closet—after all, the CEO personally bought €10 million worth of shares last September. The only plausible explanation for the current discount is modest profitability. However, HelloFresh is in a unique position to benefit from economies of scale, and it seems only a matter of time before it outcompetes its rivals and significantly boosts its bottom line. We’re issuing a Buy recommendation. As a preliminary price target, we once again set €13 per share—and even at that level, we believe the stock remains undervalued.

The author holds a long position in HelloFresh.

Auteur heeft op moment van schrijven een positie in HelloFresh.

Major Shareholders

Active Ownership Corp SARL: 7.7%

Dominik Richter (CEO): 5.0%

Key Data

Name: HelloFresh

Ticker: HFG

Sector: Food – Retail

Exchange: IBIS (Germany)

ISIN: DE000A161408

52-week low: €4.42

52-week high: €13.92

Share price: €7.78

Shares outstanding: 162 million

Market capitalization: €1.3 billion

Cash position: €0.5 billion

Total debt: €0.9 billion

Net debt: €0.4 billion

Enterprise value (EV): €1.7 billion

EV/revenue: 0.23x

Tangible book value per share: €2.96

Price/tangible book: 2.7x

Dividend per share: €0.00

Website: ir.hellofreshgroup.com