This is a chance we simply can’t ignore. We’re looking at a company with a market cap of around €2.5 billion, while one of its divisions is about to be sold for a stunning €2.3 billion in cash. That means investors are set to receive a substantial portion of their investment back through a special dividend. And the best part? The company’s profitable growth engine – its B2B division – remains entirely under Playtech’s control. What’s left is a healthy, cash-rich tech company with a strong foothold in regulated gambling markets and plenty of room for further growth.

Founding

Playtech was founded in 1999 in Estonia by Israeli entrepreneur Teddy Sagi. Together with a team of software developers, multimedia experts, and professionals from the casino industry, he developed a comprehensive software platform for online gambling. From the outset, the company focused on B2B services, providing technology to online casinos, poker rooms, bingo sites, and sports betting platforms. Although Playtech was established in Estonia, it had an international outlook from the beginning and quickly expanded throughout Europe. The decision to go public in the UK was strategic: London offered an attractive platform for high-growth tech companies, including international ones. In 2006, Playtech went public, raising approximately £312 million with a valuation of around £550 million. The proceeds were used to fund international expansion, acquisitions, and continued product development. In 2007, Mor Weizer was appointed CEO—a role he continues to hold to this day. Under his leadership, Playtech has grown into one of the world’s leading gambling software providers.

Business Activities

Today, Playtech is a major global technology supplier to the gambling industry, offering a wide range of products and services. The company provides software solutions for both online and land-based casinos, sports betting, poker, bingo, lotteries, and live casino games. A key component of its offering is the IMS platform (Information Management Solution), which allows clients to manage all player data, payments, marketing, and game content from a single system. Playtech also operates dedicated live casino studios and develops its own slot machines and table games. Sports betting technology is offered through its subsidiary, Playtech BGT Sports.

In addition to its B2B services, Playtech also operates B2C activities. Through its subsidiary Snaitech, the company offers gambling services directly to consumers in Italy, both online and in physical outlets.

Sale of Snaitech

In September 2024, Playtech announced the sale of its entire stake in Snaitech to Flutter Entertainment for €2.3 billion in cash. Snaitech is Playtech’s B2C arm, active in Italy in both online gambling and retail sports betting. The deal is expected to close in the second quarter of 2025. The sale aligns with Playtech’s strategy to fully focus on its fast-growing and highly profitable B2B operations. By divesting Snaitech—which is more capital-intensive and less scalable—the company sharpens its focus on technology and platform services for regulated gambling markets worldwide.

Caliplay Agreement

Also in September 2024, Playtech announced a new strategic agreement with Caliplay, its joint venture with Caliente in Mexico. The collaboration is being restructured, giving Playtech a 30.8% stake in a new U.S.-based holding company called Cali Interactive, which will focus on the rapidly growing regulated gambling market in the United States. The agreement ends a years-long legal dispute over contract terms and outstanding payments. For Playtech, the deal means direct revenues from Caliplay service fees will cease, but it gains the prospect of dividend income from Cali Interactive and a strategic position to participate in U.S. market growth.

2024 Results

On March 27 (pre-market), Playtech reported its full-year 2024 results. The B2C division—mainly consisting of Snaitech—saw only 2% revenue growth. Margins were around 24.5%, lower than in B2B, and future growth is limited due to market saturation and increased regulation. The B2C model is also capital-intensive, requiring investment in retail outlets, marketing, and absorbing the risk of sports results. While Snaitech remains profitable, it offers limited scalability and few international expansion opportunities. In contrast, the B2B division performed strongly. In 2024, B2B revenue rose by 10%, and EBITDA grew by 22%, with the margin increasing to 29.4%. Growth was driven primarily by North and South America, including a doubling of revenue in the U.S. Client concentration also improved: the top five customers accounted for 42% of revenue in 2024, down from 51% a year earlier—making the revenue base more stable and less reliant on a handful of large clients. Looking ahead, management expects adjusted EBITDA of €250 to €300 million from 2025 onwards, with annual free cash flow of €70 to €100 million. These figures reflect only the remaining B2B operations, as Snaitech is being sold and Caliplay is now a minority holding.

Growth in Online Casinos

Both Europe and the United States are experiencing strong growth in the online gambling market, creating attractive opportunities for Playtech. According to a recent report by the EGBA and H2 Gambling Capital, Europe’s gambling market reached a gross gaming revenue of €123.4 billion in 2024, up 5% from 2023. Online gambling was the main driver, increasing by roughly 12% to €47.9 billion. Online now represents 39% of the total gambling revenue in Europe. This growth has been fueled in part by the legalization and regulation of online gambling in countries such as Germany and the Netherlands, where online casinos are gaining popularity and taking market share from land-based venues. The U.S. online gambling market also continues to expand rapidly, according to the State of the States 2024 report by the American Gaming Association. In 2023, the U.S. gambling market posted record revenue of $66.6 billion, a 10% year-on-year increase. While traditional casinos still account for the largest share—around $49.4 billion—it is the new formats like online sports betting and online casinos that are growing fastest. Online casino games generated $6.17 billion in revenue, a 28% increase from the previous year, driven by continued legalization and regulation at the state level.

Strategy

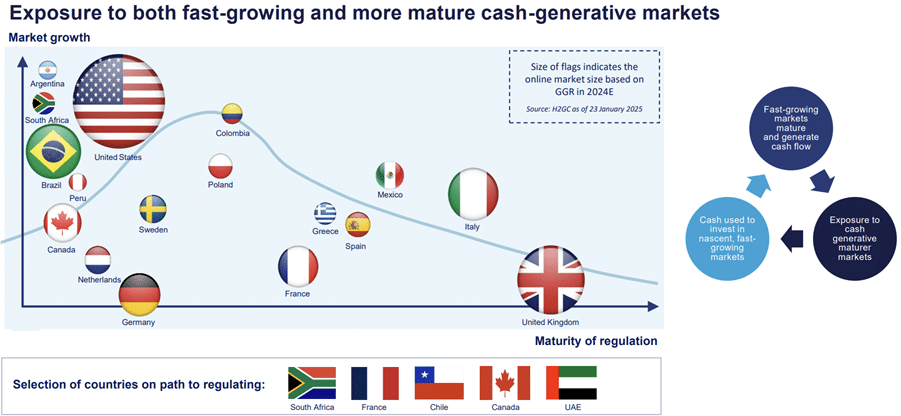

Figure 2. Playtech’s global B2B strategy. Source: Playtech.

Figure 2. Playtech’s global B2B strategy. Source: Playtech.

In its 2024 investor presentation, Playtech emphasizes that its B2B strategy focuses on balancing exposure between fast-growing markets and more mature, regulated markets. The company uses cash flow from established regions to strategically invest in emerging jurisdictions that are still in the early stages of regulation. This cyclical approach allows Playtech to continue expanding into new markets while benefiting from stable income streams in mature regions. At the bottom of Figure 2, several countries are listed: South Africa, France, Chile, Canada, and the United Arab Emirates. These markets are currently in the process of introducing or expanding gambling regulation. Playtech sees these jurisdictions as promising and views early strategic positioning as essential.

Impact of the Divestments

The combined impact of the Snaitech sale and the Caliplay restructuring is significant and delivers direct value to shareholders. Playtech currently has a market capitalization of approximately €2.5 billion. The sale of Snaitech alone brings in €2.3 billion in cash. At least €1.7 billion of that amount is expected to be distributed to shareholders via a special dividend. Since dividends reduce the share price by the amount paid, this implies an effective post-dividend market value of around €800 million. That remaining value reflects only the core B2B division, which independently generated €222 million in EBITDA in 2024 and continues to grow rapidly. Importantly, the dividend will be paid entirely in cash, with no new share issuance—so there is no dilution. Shareholders receive a substantial return on their investment while retaining ownership in a leaner, profitable, and well-capitalized B2B business. On top of this, Playtech’s restructuring agreement with Caliplay brings in an additional $140 million in cash, plus a 30.8% strategic stake in Cali Interactive—a new U.S.-focused platform targeting the regulated gambling market. Again: no dilution, but a stronger balance sheet and exposure to a high-growth sector.

Valuation and Dividend Outlook

Playtech shares currently trade at around €8.23. Investors are expected to receive at least €5.50 per share as a special dividend in the near term. That leaves about €2.73 in residual share value. We estimate 2024 net earnings per share at €0.28, implying a price-to-earnings ratio of under 10x on the remaining B2B business—an attractive multiple for a growing tech company with strong margins. The United Kingdom does not levy withholding tax on dividends. This means Dutch investors will receive the full gross dividend. Belgian investors, however, are subject to a 30% withholding tax under local law.

Conclusion

Based on management guidance and the 2024 results, we estimate Playtech’s 2025 net profit at roughly €85 million. Adjusted for the expected special dividend from the Snaitech sale, the remaining market capitalization of around €800 million translates to a P/E ratio below 10x. That’s a compelling valuation for a technology firm with high margins, structural growth, and a global footprint. It’s also worth noting that not all sale proceeds are being returned to shareholders. Playtech will retain ample financial flexibility to accelerate its B2B strategy. With continued growth in both European and U.S. online gambling markets, Playtech is well-positioned to benefit. Sharesunderten maintains a Buy rating on the stock.

The author holds a position in Playtech.

Key Data

Name: Playtech plc

Ticker: PTEC

ISIN: IM00B7S9G985

Sector: Casino Technology

Exchange: London Stock Exchange

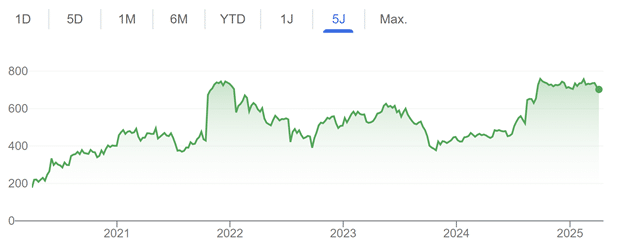

Share Price (April 1): 740 pence

52-Week Low: 432 pence

52-Week High: 775 pence

Shares Outstanding: 309 million

Market Capitalization: £2.1 billion

Estimated 2025 P/E Ratio: 9.8x

Website: https://www.investors.playtech.com/