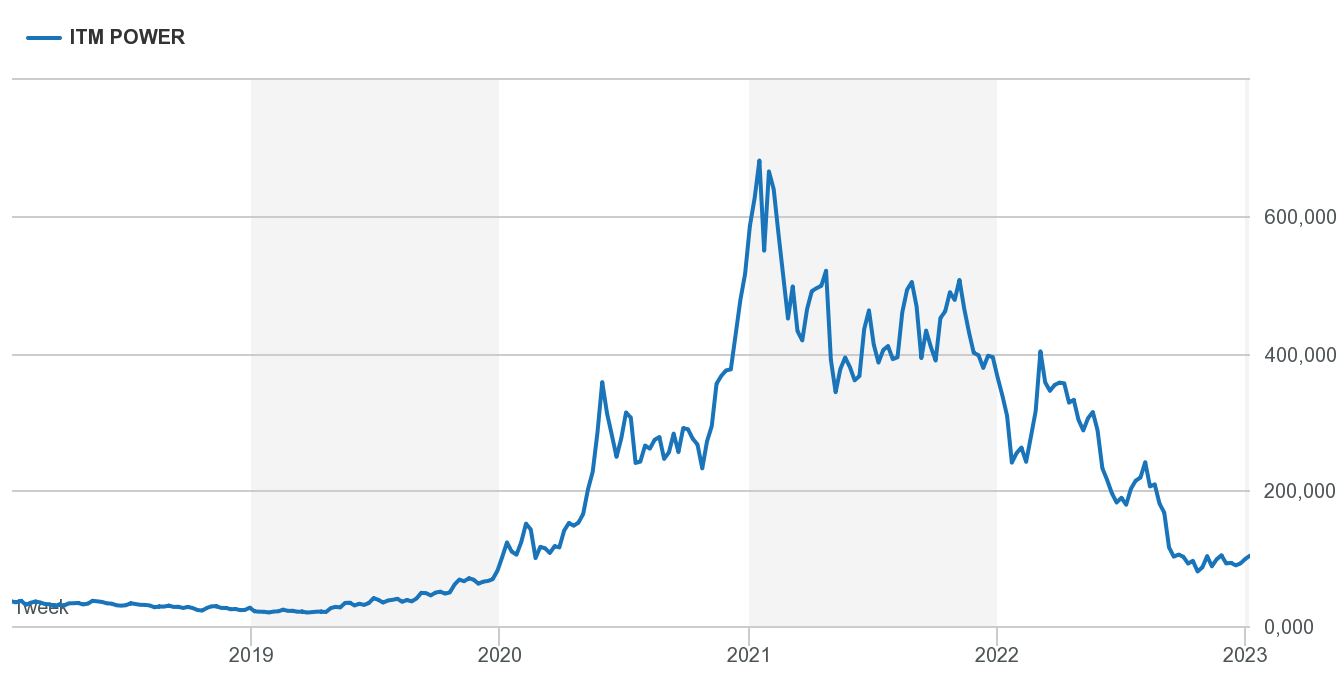

Like many other young companies, ITM Power is facing problems typical of the phase it is in. The hydrogen fuel cell producer was forced to suspend plans to build a new factory due to market uncertainty and rising costs. In addition, the latest trading update revised down the outlook for the full financial year 2022-2023, which runs until 30 April 2023. As a result, ITM Power’s share price on the London Stock Exchange has fallen from a yearly peak above 400 pence to a bottom below 100 pence.

Everything is being done to restore order as soon as possible. At the top of the company, CEO Graham Cooley stepped down and was replaced by Dennis Schulze, who earned his spurs at the German multinational Linde Engineering. Of course, it remains to be seen whether the latter will succeed in making the company profitable in the long term. Against the background of the general trend towards greater sustainability, the ITM Power share deserves some extra attention, but the risks have certainly not disappeared yet. Investors who can take a hit can nevertheless include this speculative share in their portfolio. Sharesunderonetenth takes a small position under the motto ‘nothing ventured, nothing gained’. We are therefore buying 500 ITM Power shares at the current price of around 102 GBX, which amounts to around €500. Normally we buy for around €3000.

Profile

ITM Power Plc designs, manufactures and sells hydrogen energy systems for energy storage and is therefore active in a promising sector. In recent years, interest in green hydrogen has increased rapidly worldwide and this company is responding to this with its technology. To meet the rapidly increasing demand for sustainable energy and accelerate global progress towards net zero, ITM Power has invested heavily in recent years. In 2021, the gigafactory in Bessemer Park, Sheffield, UK, was opened, which accelerated the growth of the company. Investments in new technologies and groundbreaking future-oriented solutions continue. The company’s PEM electrolysers are market leaders and will enjoy greater market penetration as the demand for green hydrogen grows. These electrolysers generate green hydrogen based on membrane technology (PEM) through proton exchange. They only require renewable energy and water, with oxygen as the only by-product. As the first hydrogen-related company to be listed on the London Stock Exchange, ITM Power is enjoying great interest from investors.

However, many shareholders are very concerned about the sharp drop in the share price since March of this year. This drop in price is in stark contrast to the sharp rise in the share price in the previous five years. ITM Power is not yet profitable and will not be for the time being. Making a profit does not seem possible for a few years. To get an idea of the speed at which the underlying business is growing, most analysts therefore look at turnover growth. In general, companies that are not yet making a profit are expected to grow their turnover every year, preferably at the fastest possible pace. In this case, expectations are met in this respect. In the past five years, ITM Power saw its turnover grow by an average of 17% per year. It is of course questionable whether this growth rate can be maintained in the future. In addition, it is important that profit is made as soon as possible. There is still a long way to go before that happens.

Numbers

Shares in ITM Power PLC have taken a further hit after the company warned in the autumn that its current financial year losses are likely to widen due to production delays. The same production delays are also putting the future of some large-scale projects at risk. It was also warned that annualised production and revenues will be at the lower end of previous expectations due to the reported production problems, and that the bottom line losses will widen. In September, management had forecast an EBITDA loss of between £45m and £50m. At that time, the pre-tax loss was already significantly higher than in the previous financial year. On the positive side, there was the news that revenues had risen by 32% to £5.6m. However, like most companies, ITM Power is currently operating in an uncertain market environment, making it difficult to provide reliable forecasts for the full financial year.

Pros:

– Active in promising sector.

– A possible huge growth potential.

– The new CEO can give the company a new impetus.

Cons:

– The share price has been very volatile in recent months.

– The company is not expected to be profitable in the next three years.

– The uncertainty about the profit evolution weighs on the share price.

Conclusion

ITM Power has had a turbulent year in 2022, with some ups but many more downs. At the time of writing, the price had not yet found a reliable bottom. That price came under extra pressure in September after ITM Power abandoned a major expansion project, another year of significant losses was predicted and CEO Graham Cooley announced his resignation. He will be replaced by Dennis Schulze, who comes from Linde Engineering, but will remain active for the company in the background. Linde and ITM Power have been working together for some time, including on a hydrogen project in Leuna, Germany. ITM Power lost just under £47 million (before tax) in the 2021-2022 financial year because it did not book any income from a large order from Linde’s hydrogen project in Leuna. However, that income could still be booked in the future. Rather than investing in a new factory in the UK, ITM Power will more than double the size of its current facility at Bessemer Park in Sheffield to 1.5 GW. The production expansion could take up to two years, but it aims to complete the job in under eight months.

A share like ITM Power should of course not be judged on the basis of the results but mainly on the basis of the forecasts. With expected investments of £30 – £40 million, the cash flow is expected to remain negative in the coming year. ITM expects the total cash burn to amount to more than £110 million this year, which is about a third of the cash that is still on the balance sheet after last year’s capital increase. It is expected that, including the current financial year, the company will continue to operate at a loss for another three years. The positive news is that ITM Power is benefiting from the significant growth in global demand for green hydrogen and therefore also from the increasing demand for hydrogen electrolysers. The expansion of production at the Bessemer Park site will help the group to reduce costs and thus accelerate the step towards profitability. The message is therefore clear: anyone who invests in ITM Power shares believes in the future of hydrogen as an alternative energy source and therefore also in this company.

Aandelenondereentientje believes that ITM Power still has a lot to prove and actually thinks it is too early to be really enthusiastic about the share. But on the other hand, we do want to anticipate the new CEO who has something to prove to the investors. Investors who can take a hit may buy a handful of ITM Power shares, but should be aware that it is a speculative and volatile share. In the portfolio of Aandelenondereentientje we therefore do it small and take a position of approximately 15% of our normal investment. In the event of a decline, we can always buy more and if we don’t see it anymore, we can also leave. So we buy 500 ITM Power shares at the current price of approximately 102 GBX under the motto ‘nothing ventured, nothing gained’.

ITM Power Fundamentals

Earnings per share 2021: –

Tax. earnings per share 2022: –

Tax. earnings per share 2023: –

Price/earnings ratio 2021: –

Price at time of writing: 94.68 pence

ISIN code: GB00B0130H42

Ticker symbol: ITM.L

Price high last 12 months: 441.38 pence

Price low last 12 months: 66.02 pence

Dividend: –

Dividend yield: –

Number of shares outstanding: 616 million

Market capitalisation: £569.82 million

Sector: Hydrogen

Return on assets: -8.14%

Return on equity: -15.76%

Website: itm-power.com