Jerome Powell indicated in his speech last week that US inflation will fall sharply this year. Powell did say that interest rates could be raised more than the market expects if employment figures or inflation turn out to be higher than expected. The markets were therefore watching today’s US inflation figure with all their eyes. Annual inflation came in higher than expected at 6.4%, versus the expected inflation of 6.2%. The StocksUnderOneTenner team is therefore curious to see whether Powell will be right and whether inflation will actually fall sharply.

The stock markets will react strongly to these kinds of figures in the coming times. According to the Aandelenondereentientje team, investors should not try to squeeze the last drop out of the barrel, because then they will often get the lid on their nose. The analyst team of Aandelenondereentientje focuses much more on the annual figures of companies and the expectations they give. We believe that this will allow us to avoid the negative market sentiment. One idea is that if you have a lot of profit on a position, you can decide to cash half of it. Then you can use the other half to search for the tops of the profit mountain.

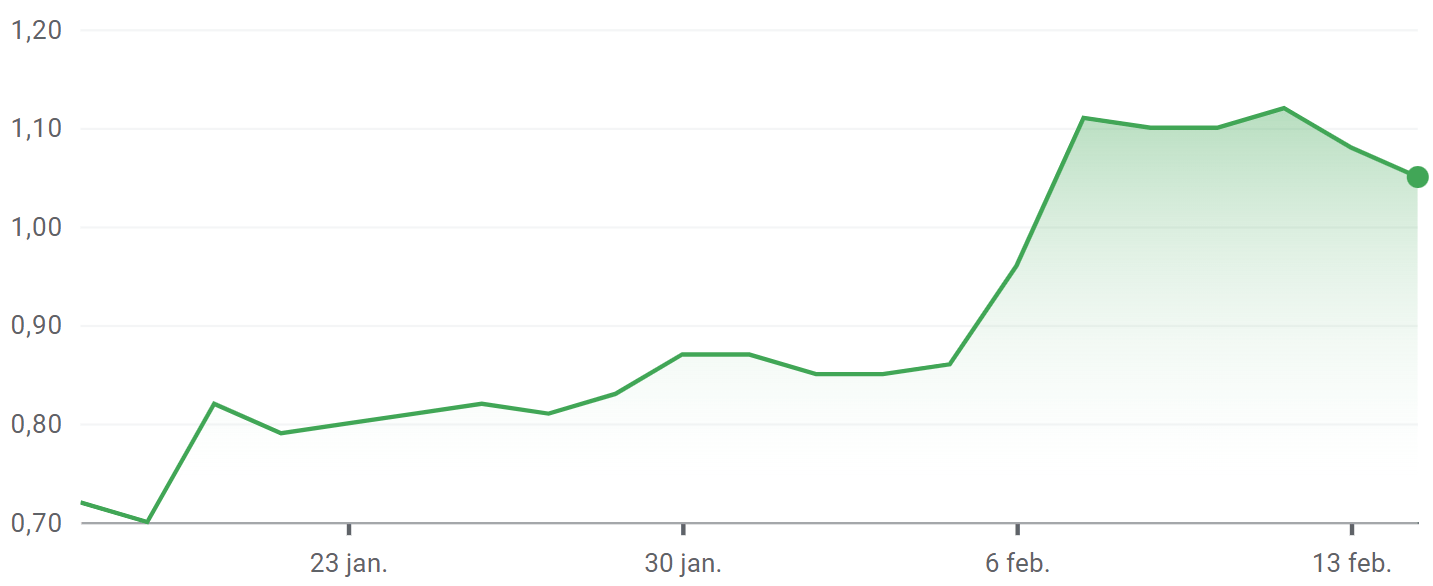

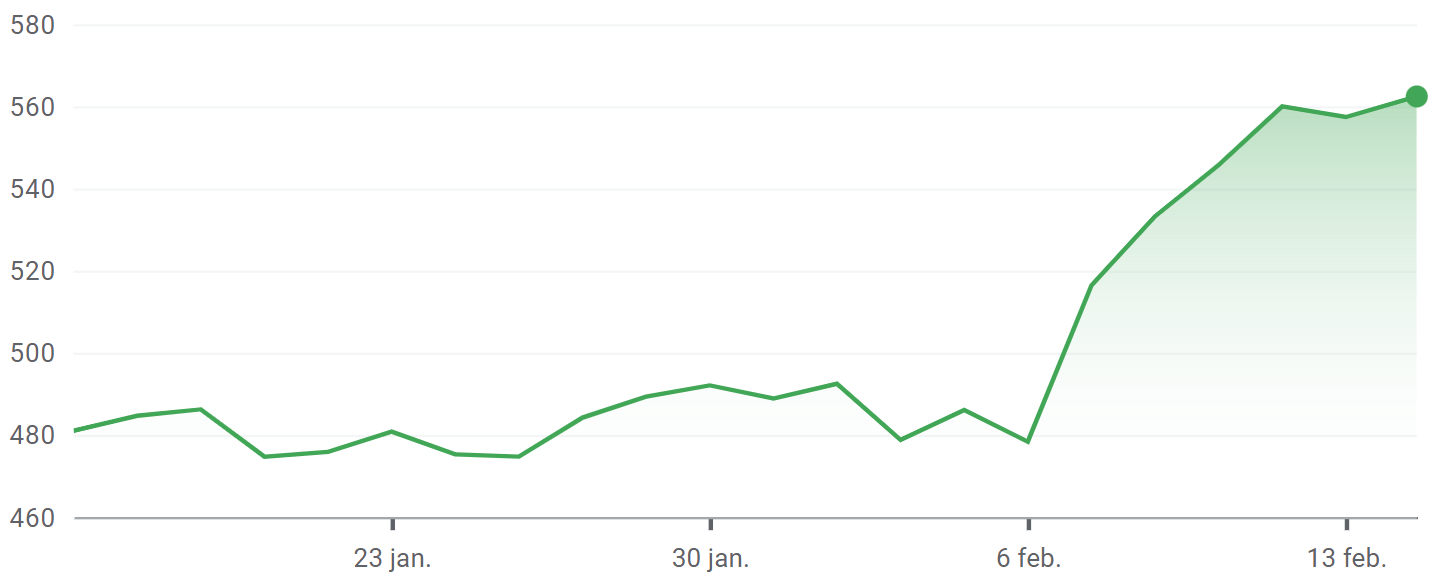

The year has started off very strong for all of us. What our analyst team is excited about are the shares under a tenner that rose sharply, such as SunLink Health Systems and BP ! We will soon come up with a new analysis of a share under a tenner. However, we would like to point out that you should limit your order, because it is a share with a market capitalization of €200 million, part of which is in stable hands. Time to discuss our portfolio.

Wallet

SunLink Health Systems : is the rightful winner of the Sharesunderatenner portfolio. You all received the analysis of this share and those who limited their order are already shining with a plus in the portfolio. The share is already more than 20% in the plus at the price we have them in the books for. The analyst team of Sharesunderatenner expects a comeback of this share and uses a higher price target. We are therefore holding the shares.

BP: the share price of this beautiful oil giant got a huge boost due to great figures and positive outlook . The share is now trading at its highest point in the past four years, which we are very happy about! The group booked a record profit of $27.7 billion last year, versus a profit of $12.8 billion a year earlier. This was mainly due to the high energy prices. The company is rewarding its shareholders enormously and is increasing the quarterly dividend by 10%. In addition, the oil giant also announced a share buyback of more than $2.75 billion. As if this was not enough, BP also reduced its debt to $21.4 billion last year. BP is also taking steps to make the world cleaner and greener, for example it wants to reduce the production of hydrocarbons and have 50 gigawatts of renewable energy in 2030. It is increasing oil and gas production and has lowered the target to reduce emissions. “We need continued investment in the current energy system – which is dependent on oil and gas – in the short term to meet today’s demands and ensure an orderly transition,” said BP’s CEO. The team at SharesUnderOneTenty expects the entire sector to remain positive and considers BP to be one of the better stocks in this sector. We therefore opt to hold the stock.

Nokia: the share price of this Finnish company has been swaying lately and according to the Aandelenondereentientje team, that is very unfair! The company is growing steadily and showed neat figures again . The group grew by 6% last year to a net turnover of €25 billion. The profit per share also rose to no less than €0.75 compared to a WPA of €0.29 a year earlier. With these good figures, Nokia also wants to reward the shareholders considerably and is increasing the dividend by more than 40% to a dividend of €0.12 per share. The Aandelenondereentientje team can therefore do nothing but state that this share should be a ‘must have investment’ in every portfolio and is holding on to the shares.

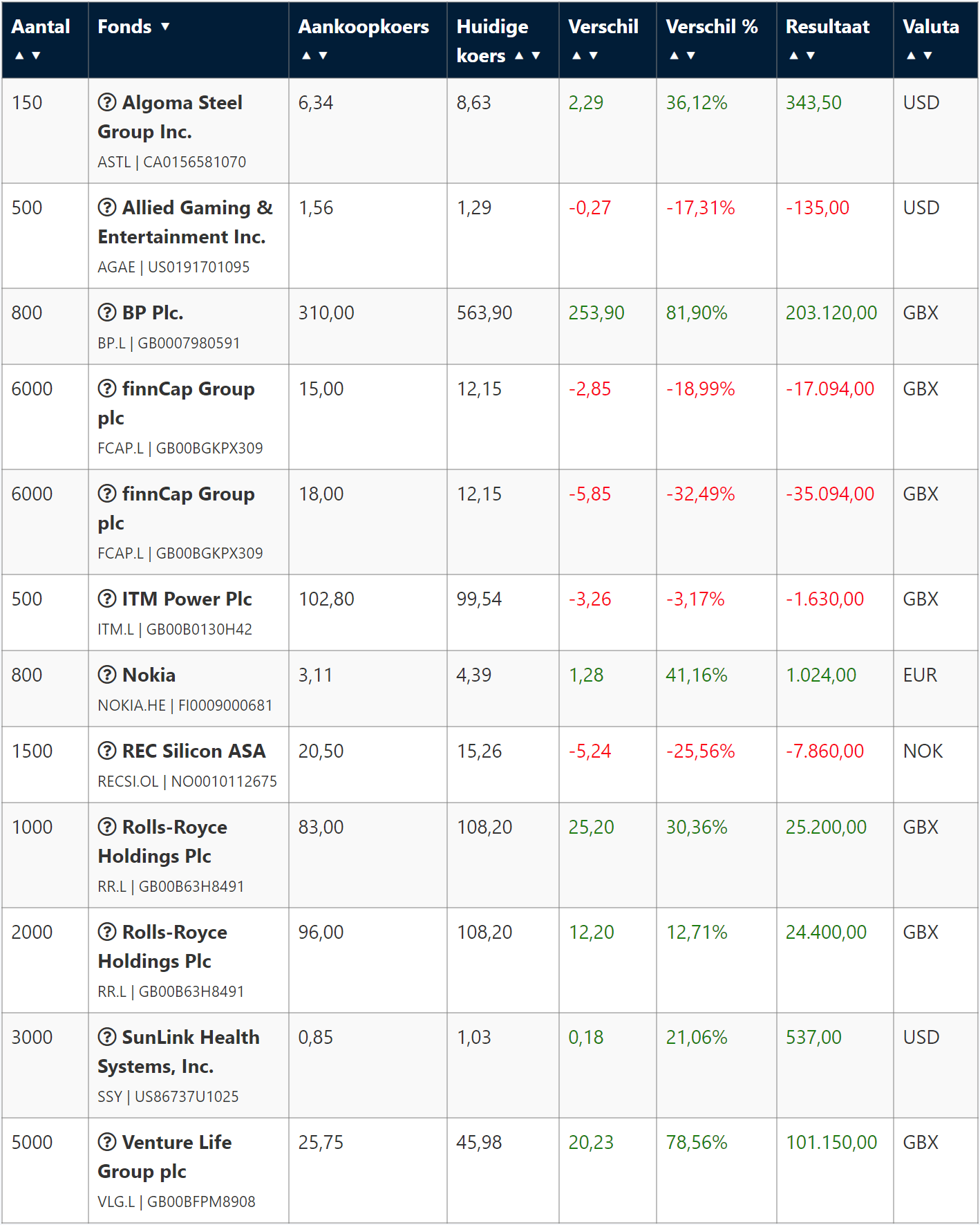

Finally, the portfolio overview: