The year 2022 was a great year for the members of Aandelenondereentientje, but the worst year since 2008 for the American stock markets. The S&P500 lost more than 19% and the Nasdaq did even better and showed a loss of 33%, with the result that some shares are at their lowest price ever. Will 2023 be the year of recovery? The Aandelenondereentientje team thinks so, but that will probably take place in the second half of the year.

Investors have at least started the new year well and an old stock market wisdom states that the sentiment for the entire year is determined by the first weeks of January. We can count ourselves lucky if the positive sentiment on the stock markets continues, but we have our doubts. The first week of the new year started off very strongly, thanks to lower interest rates, a better-than-expected German inflation report (8.6%), falling oil prices and positive figures on the service sector from the Eurozone and Germany. With this, investors hope that the inflation peak is behind us and that the European economic contraction is less severe than feared. Our team of analysts warns that investors should not cheer too soon, because we first want to see whether the inflation peak is indeed over and that the economy does not shrink any further.

Then there were the minutes of the Federal Reserve (Fed) last Wednesday evening. They do not predict much good for the rest of this year. The Fed does not plan to lower the interest rate this year, but does plan to raise the interest rate to get inflation down. Investors were already taking this into account to some extent, since the stock markets and currencies hardly reacted to this message. The team of Aandelenondereentientje sees it as follows: We think that the interest rate can go up, but only for the short term and at the end of the year the interest rate decreases will become visible again. Our reasons for this are a slower economy that then needs a boost, that many countries around us cannot afford the higher interest rate, and that inflation is falling, which eliminates the need to slow down the economy.

All in all, we anticipate a very volatile year. But we are full of ambition and the stocks we choose this year must be a hit! We have only one goal and that is to score with the penny stocks. That does not have to happen every week; better a missed opportunity than a failed opportunity. We are going for it and are convinced that the roses on the stock exchange will bloom for us! We wish you all a good year.

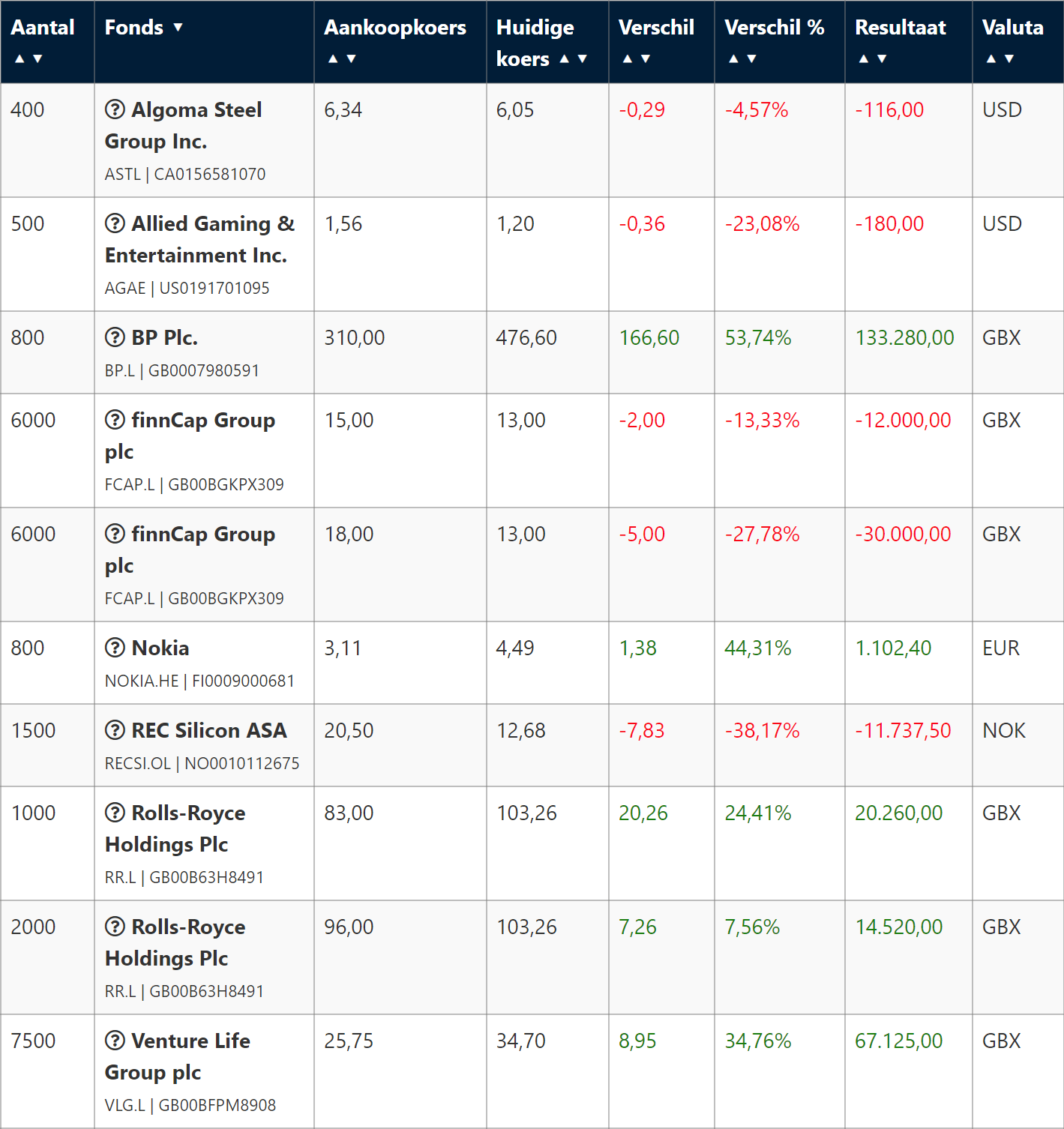

Wallet

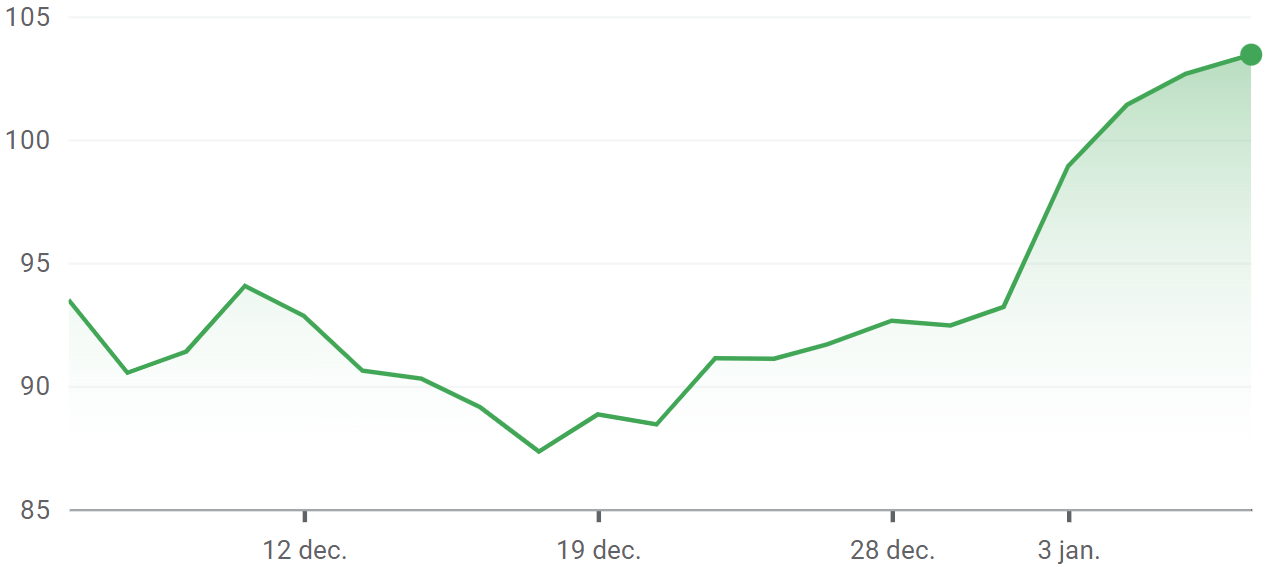

Rolls-Royce: apparently listened to us well with that 2023 may be the year for Rolls-Royce! The price has already risen by more than 10% in the first 5 days of this year. Hats off to the investors who recently bought the shares and/or already owned them. Our advice is: Hold on tight.

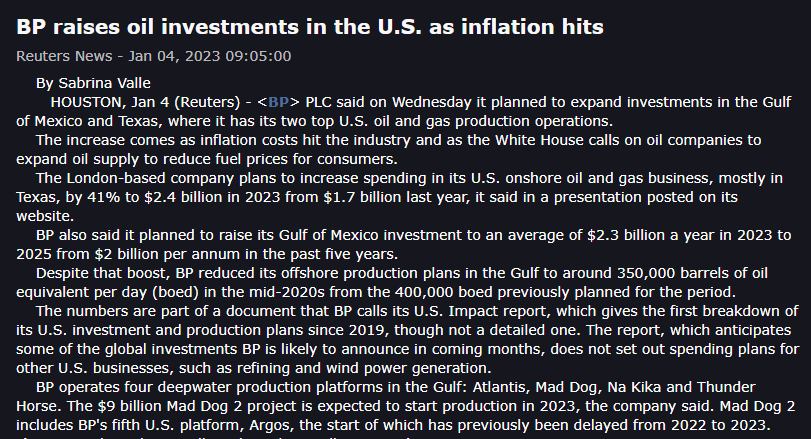

BP: Oil prices have been under heavy pressure for some time now and that is bad news for oil-related stocks, but good for falling inflation. Investors are therefore selling oil stocks, but we remain completely confident in BP as a company. The price is also barely reacting to falling oil prices. According to our team of analysts, this is a sign to be extra positive about this stock and we are significantly raising the price target from 500 GBX (British Penny) to 600 GBX. The company said last Wednesday that it will expand investments in the Gulf of Mexico and Texas, where BP has its main oil and gas activities. BP is expanding these as inflation is hitting the industry and the White House is calling on oil companies to expand oil supplies to lower fuel prices for consumers. This stock remains a must-have in any well-diversified portfolio.

The analyst team of Aandelenondereentientje already has its eye on the first share under a tenner of the new year. Our analysts are busy with the analysis and as soon as it is ready, it will be sent to you by e-mail! Finally, below is the portfolio overview.