The stock markets remain in the “winning mood”. The American inflation figures have been processed so far and, as we saw earlier, they can cause considerable price fluctuations. The reason for the sharply rising stock markets was mainly due to weakening inflation worldwide. American inflation fell last month, but as expected and came to an annual inflation of 6.5%. The monthly core inflation did rise to 0.3%, but this was also in line with expectations. According to our team of analysts, the stagnating inflation figures could well mean the end of the sharply falling inflation and we doubt whether this downward trend will continue.

The stock markets are very much ahead of the facts and if inflation starts to rise again in the coming period, the stock markets could take another big hit. Our team of analysts is therefore very curious to see how the FED views these inflation figures and whether interest rates will actually be raised significantly. Our team of analysts thinks so, but predicts a falling interest rate towards the end of this year. The American banks kick off with the figures for the fourth quarter season on Friday afternoon and that could still cause some movement. They indicated that they expect a recession, which makes them take a sober view. This is in contrast to Shares Under a Tenner, because our team of analysts has once again set their sights on promising shares under a tenner and we expect that 2023 will be the best year ever for subscribers of Shares Under a Tenner!

For those investors who still hold Smiths News shares, congratulations on the nice profits and dividend received. The Aandelenondereentientje team may enter this share later if the share price drops further, otherwise we are out of luck and enjoy the decent profits and dividends we have already received.

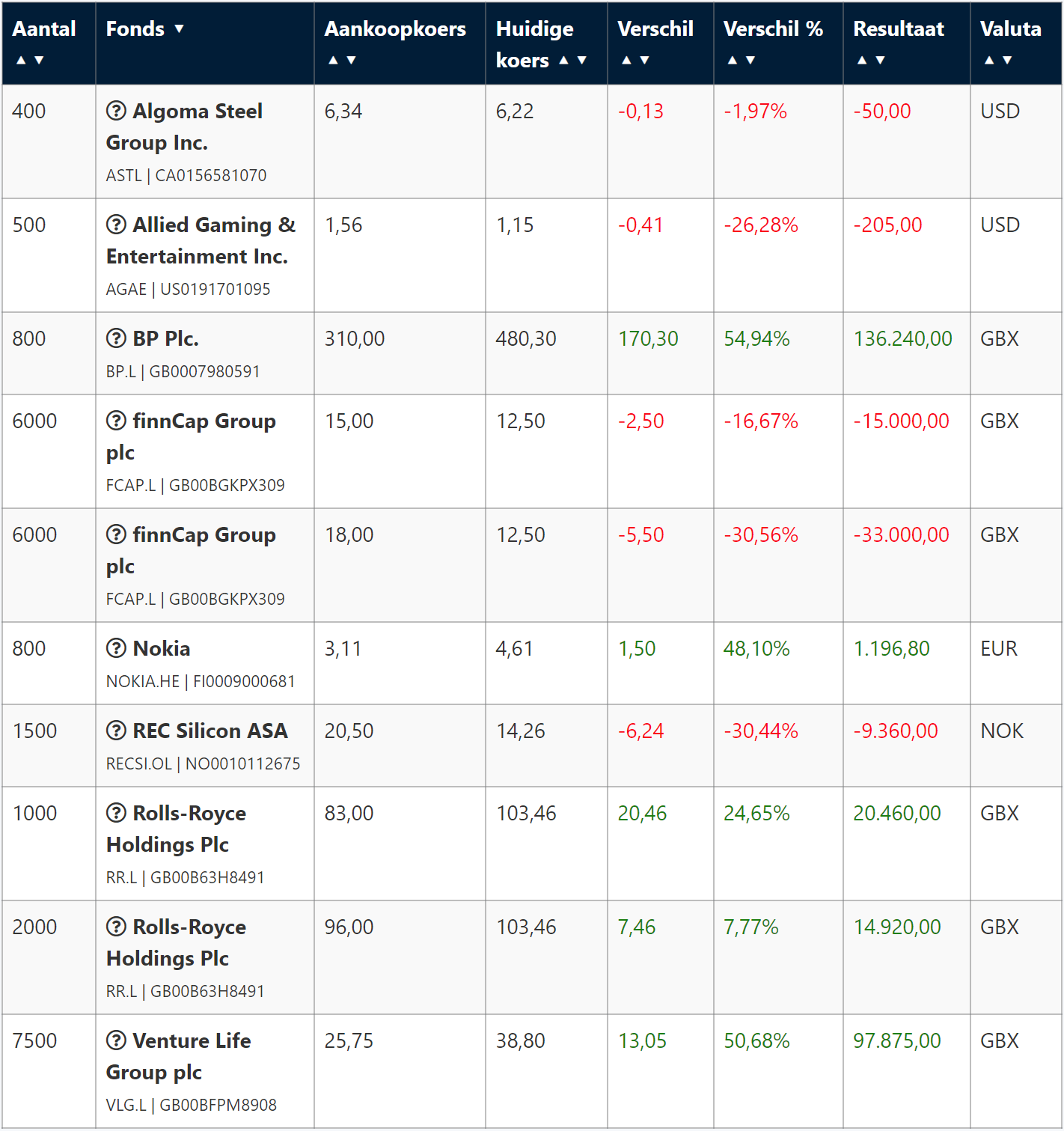

Time to discuss our portfolio. For example, we are selling a third of our position in Venture Life Group plc.

Wallet

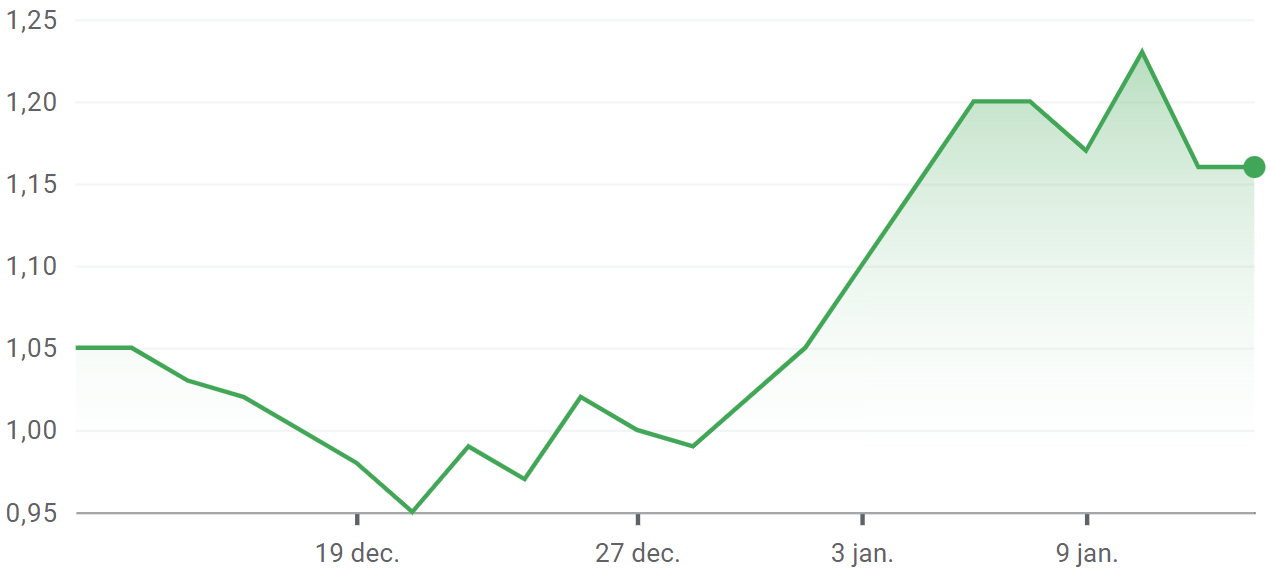

Allied Gaming & Entertainment Inc: In our opinion, this stock has been unfairly punished after the company announced that it will focus more broadly than just the “Esports” branch. The company wants to do this by focusing on the entire gaming sector and has therefore implemented a name change. Investors do not like new things that bring uncertainty and therefore sold Allied shares en masse. Our team of analysts believes that management has taken a good step with this and expects a real comeback of this stock this year. The new year has already started well, because the price has already risen around 30% in one month! Hats off to those who stayed behind. We are holding on to the shares firmly.

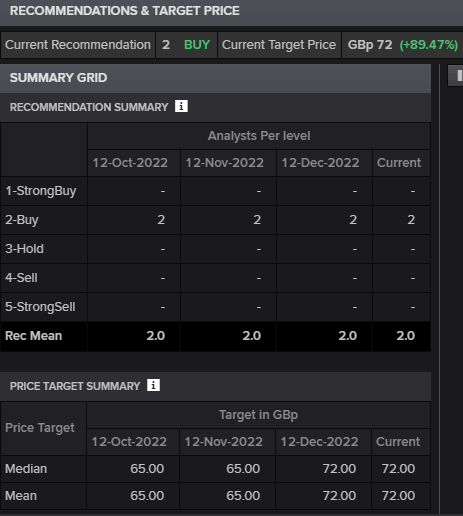

Venture Life Group plc: With this beautiful share we have made another great homerun of around 50%. We are going to sell 2500 shares and the 5000 shares that we keep will be a lot cheaper. The price jump started with the news that Venture Life Group has acquired the company HL Healthcare , which has given them three new successful ear, nose and throat labels. The price continues to rise and at the time of writing is even 7% higher. We are not alone in our view, other analysts predict an average expected price increase of around 90% to GBX 72.

Rolls Royce Holdings plc: The share has now crept above 100p. Our expectations are high and we are not thinking about realising the profits yet. We feel more than fine with this share!

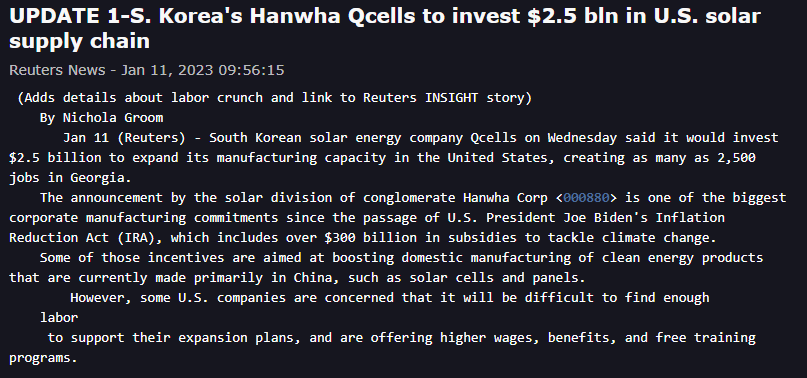

REC Silicon ASA: What a bouncy ball this stock is. When we emailed the analysis of this stock, a message came out that the Korean company Hanwha took a 16.67% stake in this Norwegian company, which was a kick-off for starting up factories in the United States. The Korean Hanwha sees a lot of growth opportunities in America and is even investing $2.5 billion in the American solar energy supply chain. This is an important step for the solar energy companies and we expect the Norwegian company REC Silicon to benefit greatly from this. Subscribers who do not yet have shares in REC Silicon can still safely step into this bouncy ball.

Finally, the portfolio overview

We have a small portfolio now, but we are going to change that! We expect more fireworks in the coming period and want to score this year. A mobile stock exchange can help us perfectly with that, so fasten your seat belts.